Table of Contents

- I. Welcome, Future Investor! – Starting Your Mutual Fund Journey in India

- II. What Exactly is a Mutual Fund? – The Basics for Indian Investors

- III. Understanding NAV – Your Mutual Fund’s “Price Tag”

- IV. Understanding AUM – The Total Size of a Mutual Fund

- V. NAV vs. AUM: The Core Differences Explained for Beginners

- VI. Why Do NAV and AUM Matter to YOU, the Indian Investor? – Making Smart Decisions

- VII. Avoiding Common Mistakes – Learning from Others’ Experiences

- VIII. Tools and Resources for Indian Mutual Fund Investors

- 1. Online Platforms Making Investing Easy (Specific Indian Examples)

- 2. Tracking Your Investments: Staying on Top of Your Portfolio

- 3. Learning More: Resources for Continuous Growth and Investor Education

- A. AMFI’s “Mutual Funds Sahi Hai” Campaign: Simple Explanations and Videos

- B. SEBI Portal for Investor Education: Understanding Your Rights

- C. Financial Advisors: When to Seek Professional Help and Where to Find Registered Ones in India

- D. Monthly Factsheets and Their Benefits: Understanding Detailed Fund Reports

- IX. What Beginners Should Focus on Instead of Just NAV and AUM

- X. Conclusion – Your Path to Financial Confidence with Mutual Funds

- XI. FAQs about differences between NAV and AUM in Mutual Funds

- 1. What is the main difference between NAV and AUM in simple words?

- 2. Does a higher NAV mean better returns or a more expensive fund?

- 3. How often is NAV updated and published for Indian mutual funds?

- 4. Where can I find the latest NAV and AUM of any mutual fund in India?

- 5. What is considered a good AUM for a mutual fund?

- 6. Can a fund's AUM decrease? If yes, what are the common reasons?

- 7. Is it generally safe to invest in a fund with a very low AUM?

- 8. How does a fund's AUM size indirectly affect my investment returns?

- 9. Should I choose a mutual fund scheme purely based on its NAV?

- 10. How does SEBI (Securities and Exchange Board of India) ensure correct NAV and AUM reporting?

Today, more Indians are turning to mutual funds to grow their savings.

As you explore this path, you’ll come across terms like NAV (Net Asset Value) and AUM (Assets Under Management). Understanding the differences between NAV and AUM in mutual funds in India is key to making informed investment choices.

This article breaks down what NAV and AUM mean, how they affect your investments, and why knowing them helps you build a stronger financial future.

We’ll walk through real-life examples, practical tools used in India, and common mistakes to avoid.

Whether you’re just starting out or looking to sharpen your knowledge, this guide will help you build confidence in your mutual fund decisions.

Let’s begin!

I. Welcome, Future Investor! – Starting Your Mutual Fund Journey in India

1. Investing Made Easy: Why Mutual Funds Are Great for You

A. Taking Control of Your Money: Simple Steps to Financial Growth

Let’s say you want to save up for your child’s college or maybe plan a small family vacation. If you just keep that money in your savings account, it won’t grow much — and inflation will slowly eat into its value.

That’s where mutual funds come in.

Mutual Funds help your money grow by investing it smartly.

Think of it like this:

Instead of investing alone, many people like you come together and pool their money. That big group of money is then used to buy things like company shares, government bonds, or even gold.

You don’t have to do all the work yourself. Experts called fund managers take care of everything for you. They decide which stocks or bonds to buy or sell so you can focus on your goals.

B. Why Mutual Funds are a Smart Choice for Indian Savers

In India, most people start with fixed deposits (FDs) or Public Provident Fund (PPF), which are safe but give limited returns.

Mutual funds can give better returns over time — especially if you choose the right kind.

For example:

- If you’re saving for a short goal like buying new furniture before Diwali, you might go for a debt fund.

- If you’re saving for your child’s education 10–15 years from now, an equity fund might be better because it has more growth potential.

And here’s the good news — you don’t need to be a finance expert to get started.

All you need is a smartphone and a few minutes. Platforms like Zerodha, INDMoney, Groww and Kuvera make it super easy to invest from home, without any paperwork or long queues.

I remember my friend, who started investing ₹2,000 every month through Kuvera. He didn’t know much about markets at first, but he picked a simple index fund. In 3 years, his money grew by nearly 40%! He stayed consistent and let his money work for him.

So whether you’re planning a trip, building a house, or saving for retirement, mutual funds can help you reach your goal faster than just keeping money in a bank.

A. Demystifying Jargon: Making Sense of Investment Words

When you start reading about mutual funds, you’ll hear terms like NAV (Net Asset Value) and AUM (Assets Under Management). At first, they may sound complicated, but they aren’t.

- Think of NAV as the price of one unit of the fund — like the price tag of a product you buy.

- AUM tells you how big the fund is — how much total money is invested in it.

Once you understand these two numbers, you’ll know more than most beginners and can make smarter investment choices.

B. Building Confidence: Your First Steps Towards Smart Investing

I am going to explain everything step by step. No jargon. No confusion. Just plain, simple language that anyone can understand.

By the end of this article, you’ll not only know what NAV and AUM mean, but also how they affect your investments and how to use them to pick better funds.

The numbers of NAV and AUM tell you different things:

- NAV shows how much each unit of your fund is worth today.

- AUM shows how big the fund is overall.

Both are important in their own way.

For example, if you’re investing in a new fund with very low AUM, you should be careful — sometimes newer funds carry more risk. Or, if you see a high NAV, don’t think it means the fund is expensive — it’s not like buying a costly stock.

Knowing these basics helps you avoid common mistakes and gives you the confidence to invest wisely.

So, let’s begin and learn exactly what NAV and AUM are, how they work, and why they matter to you, an Indian investor.

II. What Exactly is a Mutual Fund? – The Basics for Indian Investors

1. Imagine a Money Pool: How Mutual Funds Work in India

A. Small Savings, Big Impact: Pooling Money with Other Investors

Let’s say you and your neighbor both want to grow your savings. If you try investing alone, it may not feel like much. But if thousands of people like you come together and pool their money — that’s a big amount!

That’s exactly how mutual funds work!

Think of a mutual fund like a big group fund where many small investors, like you and me, put in money. This pooled money is then used to buy things like:

- Shares of Indian companies (like shares of Reliance, Infosys, etc.)

- Government bonds (safe loans to the government)

- Gold (through gold ETFs)

As the value of these assets goes up, so does your investment.

Once you’ve reached your financial goals, or if you ever need funds, you have the flexibility to sell all or part of your mutual fund units. You can do this at your convenience, or according to the mutual fund’s guidelines.

For example:

- If you invest ₹5,000 in a mutual fund, you’re not buying just one stock or bond. You’re getting a small share in a large collection of investments. That helps reduce risk and gives you better chances to grow your money.

B. Who Manages Your Money? Understanding Fund Managers and AMCs (Asset Management Companies)

You might be wondering — who looks after all this money?

Your money in mutual funds is not left alone. It’s managed by professionals called Fund Managers. These are experienced people who make decisions on what to buy and sell in the market.

They work for companies called AMCs (Asset Management Companies). Some well-known AMCs in India are:

- HDFC Mutual Fund

- ICICI Prudential Mutual Fund

- SBI Mutual Fund

These fund managers study the markets, track company performance, and decide which stocks or bonds to invest in — all based on the fund’s goal.

So even if you don’t know much about the stock market, you can still invest confidently because there’s someone experienced doing the hard work for you.

2. Different Flavors of Mutual Funds: Finding Your Perfect Match

Now that you know how mutual funds work, let’s look at the different types available in India.

Just like how we choose between tea and coffee based on taste, you can pick a mutual fund based on your goals and comfort with risk.

Here are the main types:

A. Equity Funds: Investing in Indian Companies for Growth

Equity funds mostly invest in shares of Indian companies listed on exchanges like NSE or BSE.

If you’re okay with some ups and downs and want good returns over the long term (say, 5–10 years), equity funds could be right for you.

For example:

- If you invested in an equity fund 7 years ago, say in HDFC Equity Fund, your money might have grown by around 12–15% every year on average.

Equity funds are great for big goals like:

- Buying a house

- Funding your child’s education

- Retirement planning

Just be aware that the equity funds have higher risk for short-term periods. However, when you look at the bigger picture, these funds generally offer better returns compared to others over the long term.

B. Debt Funds: A Safer Bet with Indian Government Bonds and Company Loans

Debt funds invest in fixed-income instruments like:

- Government bonds (safe, backed by the government)

- Company deposits (like FDs but traded in the market)

- Treasury bills

These funds are less risky and give more stable returns. They are perfect for short-term goals (up to 3 years).

For example:

- If you’ve saved ₹2 lakh for your next Diwali shopping or a family trip, putting it in a debt fund instead of a savings account might help it grow a little faster without taking too much risk.

Debt funds are great for short term goals like:

- Going on a vacation

- Purchasing a new phone

- Saving emergency funds

C. Hybrid Funds: A Mix of Both for Balanced Growth

Hybrid funds are like a mix of tea and milk — a bit of equity and a bit of debt.

They balance growth and safety, making them ideal if you want steady returns without too much worry.

There are two common types you’ll find:

- Aggressive hybrid funds: These have more equity (around 65%), along with some debt. They aim for higher growth but come with slightly more risk.

- Conservative hybrid funds: These focus more on debt, with a smaller portion in equity. They offer more stability and are good if you prefer less risk.

For example:

- Let’s say you have a goal like buying a car in 4–5 years. A hybrid fund could help you grow your money steadily without risking everything, offering a middle ground between pure equity and debt.

Hybrid funds are great for goals like:

- Saving for a down payment on a car (medium term)

- Planning for a home renovation

- Building a balanced portfolio for moderate risk appetite

D. Other Types: Gold Funds, Index Funds, and More

Besides the main types like equity, debt, and hybrid funds, there are a few more kinds of mutual funds you can explore:

- Gold Funds: These funds follow the price of gold. You don’t have to buy physical gold — your money is invested in gold through these funds. They’re useful for balancing your portfolio, especially when prices rise due to inflation.

- Index Funds: These funds track popular stock market indexes like Nifty 50 or Sensex. They simply copy the performance of these indexes, making them a low-cost and easy way to invest in the stock market.

- Sector Funds: These focus on specific sectors like banking, pharma, or IT. If that particular sector does well, these funds can give good returns. But they also carry higher risk since they don’t spread your money across different areas.

- ELSS Funds: Also called Equity-Linked Savings Schemes, these are tax-saving funds under Section 80C. They come with a lock-in period of 3 years, but they help you save tax while investing in stocks — a good alternative to options like PPF.

- International Funds: These funds invest in companies outside India — like Apple, Amazon, or Samsung. They help you spread your investments across countries and benefit from growth in global markets.

Each of these funds has its own benefits and risks. Choose based on your goals, how much risk you can take, and where you see opportunities.

Let me share a quick story.

My friend started investing in Nippon India Index Fund – Nifty Plan a few years back. He didn’t want to spend time picking stocks, so he chose an index fund that follows the Nifty 50. Over time, his money grew steadily without needing any daily tracking.

So whether you’re saving for a short-term goal or building wealth for the future, there’s a mutual fund for every kind of investor in India.

And the best part? You don’t need to be an expert.

With platforms like Zerodha, INDMoney, Groww and Kuvera, you can start investing from as low as ₹500 — and build your financial future step by step.

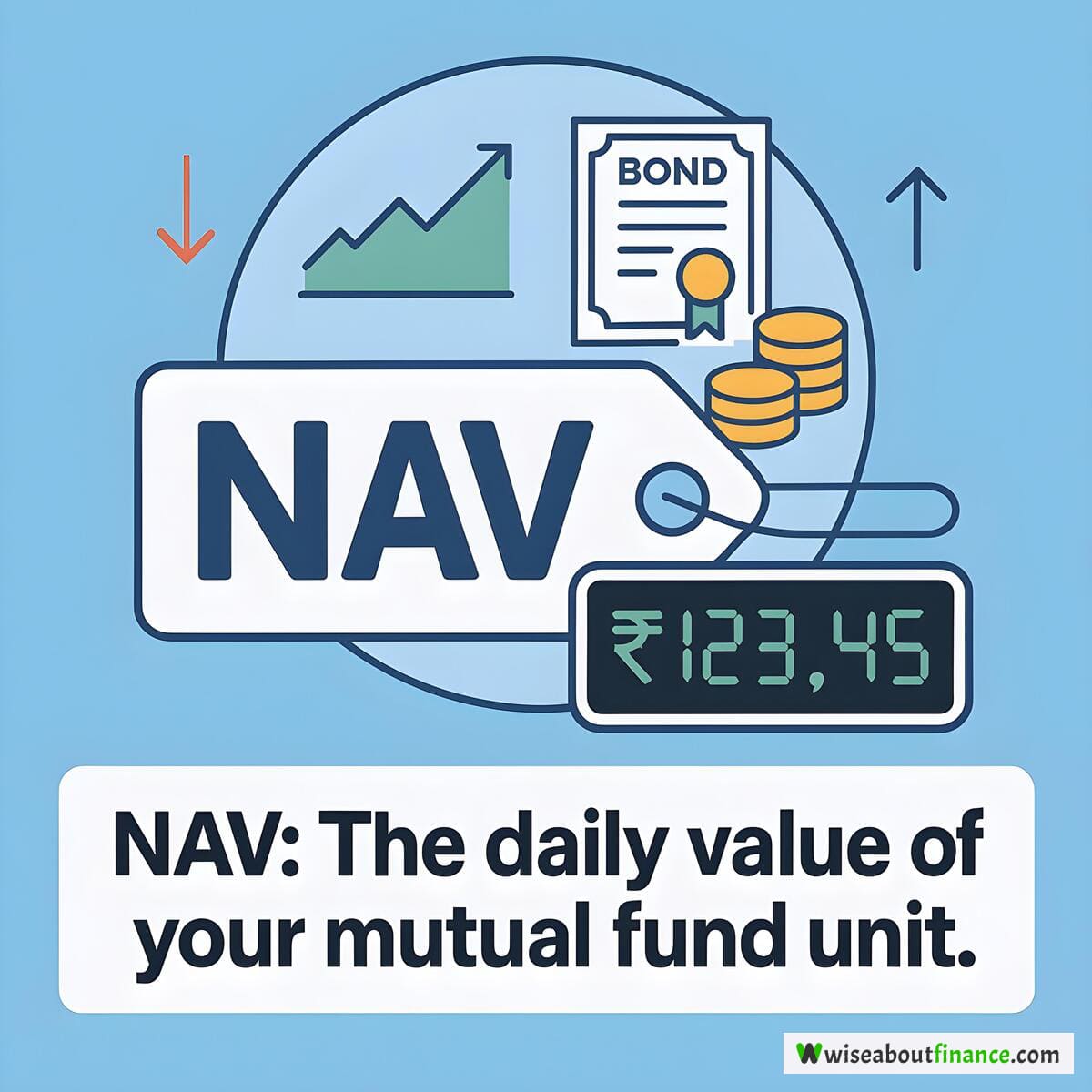

You know how you check the price of tomatoes or petrol every day because it changes often?

In mutual funds, NAV (Net Asset Value) is like that daily price tag — but for your investment.

The NAV tells you how much each unit of the fund is worth today.

For example, if a fund has a NAV of ₹50, that means one unit costs ₹50.

Let’s say you invest ₹10,000 in a mutual fund with a NAV of ₹50. That gives you:

₹10,000 ÷ ₹50 = 200 units

Now, imagine after a month, the NAV goes up to ₹60.

Your 200 units are now worth:

200 x ₹60 = ₹12,000

So, your money grew by ₹2,000 just because the NAV went up.

That’s why tracking NAV helps you see whether your investment is going up or down.

Just so you remember, NAV stands for Net Asset Value.

This is the value of all the fund’s assets (like stocks and bonds) minus any expenses or debts it has.

Think of it like this:

- If the fund owns ₹100 crore worth of stocks and other investments → that’s its total assets.

- But it also has some expenses like staff salaries and office costs → those are liabilities.

- So, what’s left after subtracting those expenses is the Net Value — and that becomes the NAV.

A. What’s Inside the Fund? Total Assets Minus Total Liabilities

Here’s how the AMCs decide the NAV:

They take:

- Everything the fund owns (total assets)

- Subtract everything it owes (total liabilities)

- Then divide that number by the total number of units people own.

The formula looks like this:

NAV = (Total Assets - Total Liabilities) ÷ Total Number of Units

B. The Simple Math: (Assets – Liabilities) / Total Number of Units

Let’s make it even clearer with numbers:

Imagine a fund has:

- ₹100 crore in assets (like shares and bonds)

- ₹1 crore in expenses (staff, audit fees, etc.)

- 1 crore units issued to investors

Then,

NAV = (₹100 Cr - ₹1 Cr) ÷ 1 Cr = ₹99 per unit

So, each unit costs ₹99 today.

C. Real-Life Calculation Example

This same calculation happens every day for big funds like SBI Bluechip Fund or Nippon India Large Cap Fund.

If you use apps like Zerodha, INDMoney, Groww and Kuvera, you can see the latest NAV updated every midnight at around 12:30 AM.

That’s when the fund house calculates the day’s value and publishes it for all investors to see.

Since mutual funds invest in things like stocks and bonds — which go up and down in value — the NAV also changes every day.

Remember this:

- If the stock market rises, the NAV goes up.

- If the stock market falls, the NAV drops.

But don’t worry too much about small daily changes. Over time, the trend matters more than one-day ups and downs.

Let’s say you start a Systematic Investment Plan (SIP) of ₹5,000 every month.

Each month, you’ll get a different number of units based on that day’s NAV:

| Month | NAV | Units You Get |

|---|---|---|

| Jan | ₹50 | 100 units |

| Feb | ₹40 | 125 units |

| Mar | ₹50 | 100 units |

Over time, you end up buying more units when prices are low and fewer when prices are high. This balances out your average cost — a smart way to invest called Rupee-Cost Averaging.

If there’s bad news in the market — like a global crisis or political uncertainty — your NAV may fall.

But if the economy improves or companies do well, the NAV will rise again.

Here’s the key tip:

Don’t panic during short dips. Stay invested and give your money time to grow.

Markets move up and down, but over the long term, good funds tend to recover and grow.

Many people think a fund with a NAV of ₹10 is better than one with a NAV of ₹100 — like buying cheaper mangoes.

But that’s not true!

What really matters is how fast the NAV grows over time.

Let’s compare two funds:

| Fund Name | Starting NAV | After 1 Year |

|---|---|---|

| Fund A | ₹10 | ₹12 (+20%) |

| Fund B | ₹100 | ₹120 (+20%) |

Both gave the same growth — 20%!

So, a lower NAV doesn’t mean it’s a better deal.

Focus on how much it grows, not how low it starts.

4. Personal Story

My friend Ravi once avoided investing in a good fund because he thought its NAV was “too high.” He later realized that fund gave 15% annual returns over 5 years — far better than many “low NAV” funds he had considered. Now he knows — it’s not about the price, it’s about the growth!

IV. Understanding AUM – The Total Size of a Mutual Fund

1. What is AUM? How Big is the Money Pool You’re Joining?

A. AUM Stands for Assets Under Management: All the Investor Money Combined

AUM (Assets Under Management) simply means how much total money is currently sitting in a mutual fund.

Think of it like this:

If you and your friends decide to start a small investment group and each person puts in ₹10,000, your group has ₹1 lakh total to invest. This means the total of ₹1 lakh is the AUM.

Now imagine that on a large scale — thousands of people putting money into a mutual fund. That total amount becomes the AUM.

So if a fund’s AUM is ₹5,000 crores, that means ₹5,000 crores worth of money from investors like you and me, is invested in that fund.

B. Why AUM Matters: Insights into Fund Popularity and Scale

A higher AUM usually shows that many people trust that fund.

For example:

- Funds like HDFC Equity Fund or Axis Bluechip Fund have AUMs in the range of thousands of crores.

- That tells us they’ve been around for a while and lots of investors are putting their money there.

But don’t just pick a fund because its AUM is big. It’s only one part of the picture.

C. Full Form of AUM: Assets Under Management

Just so you remember clearly, AUM stands for Assets Under Management — which means all the money the fund currently manages for its investors.

2. What Makes AUM Grow or Shrink?

A. New Investors Coming In: More Money Means Higher AUM

When more people start investing in a fund, the AUM goes up.

This often happens when:

- The fund gives good returns.

- It gets good reviews online or through word-of-mouth.

Let’s say a fund gives 15% returns every year for 3 years. People will hear about it and start investing more — increasing its AUM.

This kind of investment in a mutual fund, is called an Inflow, and it increases the overall AUM.

B. Existing Investors Taking Money Out: Lower AUM (Outflows)

On the flip side, if a fund doesn’t perform well, some investors may pull out their money.

When that happens, the AUM goes down.

For example:

- If a fund gives poor returns for 6–12 months, people might lose confidence and move their money elsewhere.

This kind of withdrawal is called an Outflow, and it reduces the overall AUM.

C. Fund Performance: When Investments Grow (or Shrink), AUM Changes Too

It’s not just new money or withdrawals that affect AUM.

Even if no one adds or removes money, the AUM can go up or down based on how well the fund performs.

Let’s say:

- You invest in a fund with a NAV of ₹50.

- Over time, the fund’s assets grow in value — maybe the stocks it owns become more expensive.

- So the NAV increases to ₹60.

- Automatically, the AUM also goes up — even without any new investors.

The opposite happens too — if the fund loses value, the AUM drops.

D. Real-Life Example: AUM of a Top Indian Mutual Fund

Take SBI Bluechip Fund, for example.

As of 19 Jun 2025, it had an AUM of over ₹52,251.14 crores.

That huge number shows two things:

- A lot of people trust this fund.

- It’s been around for a long time and has performed consistently.

But again, it’s not just about size. Some smaller funds may give better returns than big ones.

3. AUM in the Indian Context: What Big AUM Might Mean for Investors

A. Popularity and Trust: Large AUM Often Indicates Investor Confidence

In India, many investors feel safer investing in funds with high AUM because:

- They’re usually managed by experienced fund houses.

- They’re less likely to shut down or behave unpredictably.

- They offer better liquidity — meaning you can redeem your units easily.

But always check the fund’s performance before jumping in.

B. Management Fees: How AUM Can Affect What You Pay (Expense Ratio)

Mutual funds charge a small fee for managing your money — called the Expense Ratio.

Here’s the good news:

- Larger AUM can sometimes mean lower expense ratios.

- Because the fund spreads its costs across more investors, each investor pays a little less.

For example:

- A small fund with ₹500 crores AUM might charge 1.2% per year.

- A bigger fund with ₹20,000 crores AUM might charge only 0.8%.

That 0.4% difference may seem small, but over time, it adds up!

C. How Fund Size Impacts Investment Strategy: Big Funds vs. Small Funds

Big funds with high AUM can face challenges:

- They have more money to manage, so they can’t take risky bets easily.

- They may miss out on fast-growing small companies because buying a small stock won’t make a big difference for them.

Small funds with low AUM can be more flexible:

- They can invest in smaller companies that have growth potential.

- But they also come with more risk — especially if the fund manager isn’t experienced.

4. Personal Story

My friend Ramesh once invested in a small fund with a very low AUM. He thought it would grow faster — and it did! But after a year, the fund underperformed because the manager wasn’t experienced. He learned that AUM alone isn’t enough — he now checks the fund manager’s track record and past performance too.

So, as you explore mutual funds in India, think of AUM as a signpost — it gives you clues about popularity, stability, and cost. But never rely on it alone. Always look at performance, fund type, and your own goals.

1. The Key Difference: Price Tag vs. Total Size

Let’s break it down in a simple way:

Think of NAV like the price tag on something you buy — say, a packet of biscuits.

If a fund has a NAV of ₹50, that means one unit of that fund costs ₹50 today.

Every time you invest, you’re buying units at that day’s NAV. And when you sell, you get money back based on that day’s NAV.

This means:

Your profit or loss depends directly on the NAV.

B. AUM: The Total Wealth the Fund Manages (The Fund’s Overall Size)

Now imagine that the biscuit shop, is actually a big bakery.

AUM is like how much total flour, sugar, and butter the bakery uses to make biscuits every day — in short, how big the bakery is.

Similar to the above:

AUM tells you the total value of all the money investors have put into a fund. It’s the grand total of what every investor’s invested money is worth today.

It doesn’t tell you how much you will earn — but it gives you an idea of how many people trust that fund.

For example:

- HDFC Equity Fund has an AUM of thousands of crores.

- That shows it’s popular and trusted by many investors.

But popularity alone doesn’t mean it’s the best fund for your goal.

2. Why Both Numbers are Important (But for Different Reasons)

Here’s how each number helps you:

You check NAV to know:

- How much your investment is worth today.

- Whether you made a profit or loss since you bought the units.

Let’s say:

- You invested ₹10,000 when NAV was ₹50 → you got 200 units.

- After 6 months, NAV rises to ₹60 → your investment becomes ₹12,000.

That’s how NAV directly affects your returns.

B. Understanding Fund Scale: How AUM Shows the Fund’s Reach and Stability

AUM helps you understand:

- If the fund is popular among investors.

- Whether it’s stable enough to handle market ups and downs.

Big funds with high AUM may feel safer because they have more resources.

But small funds can sometimes grow faster if managed well.

So while AUM doesn’t affect your personal returns, it helps you decide if a fund feels reliable.

Many new investors in India make mistakes based on misunderstandings about NAV and AUM. Let’s clear them up:

Some people think a fund with NAV ₹100 is expensive, and one with NAV ₹10 is cheaper — just like thinking a ₹100 shirt is costlier than a ₹10 one.

But this is not true in mutual funds.

What really matters is how fast the NAV grows over time.

Let’s compare two funds:

| Fund Name | Starting NAV | After 1 Year |

|---|---|---|

| Fund A | ₹10 | ₹12 (+20%) |

| Fund B | ₹100 | ₹120 (+20%) |

Both gave 20% growth — so neither is better just because its NAV is lower.

For example, my cousin once avoided investing in a good fund because he thought its NAV was “too high.” Later, he realized that same fund gave solid returns year after year. He now knows — it’s not about the price, it’s about how much it grows!

B. Big AUM Isn’t Always “Better”: Focus on Performance, Not Just Size

Just because a fund has a huge AUM doesn’t always mean it’s the best choice.

Sometimes large funds can be too big to move quickly and miss out on good opportunities.

Smaller funds might be able to take smart risks and grow faster.

So, instead of picking a fund only because it has a large AUM, ask:

- Has it given consistent returns?

- Does it match my financial goals?

C. Why Confusing Them Can Mislead You: Mistakes Indian Beginners Commonly Make

Don’t fall into these traps:

❌ Mistake 1: Choosing a fund only because its NAV is low.

✅ Remember: Lower NAV doesn’t mean better returns.

❌ Mistake 2: Picking a fund only because it has a very high AUM.

✅ Check performance, fund type, and whether it matches your goals.

❌ Mistake 3: Thinking NAV and AUM are the only things that matter.

✅ Look beyond — check expense ratio, fund manager, past returns, and risk level.

| Feature | NAV (Net Asset Value) | AUM (Assets Under Management) |

|---|---|---|

| What it is | Price of a single unit of the mutual fund | Total market value of all assets managed by the fund |

| What it tells | Your investment's value per unit; your profit/loss | Fund's overall size; popularity; liquidity |

| How it changes | Daily, based on market value of underlying assets | Daily, based on investor inflows/outflows and fund performance |

| Why it matters | Tracks your personal growth; determines buy/sell price | Indicates fund stability; can influence fund manager's strategy |

By understanding the difference between NAV and AUM, you’ll avoid common mistakes and pick better funds that suit your needs as an Indian investor.

NAV plays a big role every time you invest or take your money out. Let’s understand how.

Every time you invest in a mutual fund — whether it’s a lump sum (one-time) or through a SIP (Systematic Investment Plan) — you buy units at that day’s NAV.

For example:

- You invest ₹5,000 when NAV is ₹50 → you get 100 units.

- Next month, NAV goes up to ₹60 → your ₹5,000 now gives you only 83 units.

So, always check the latest NAV before investing — especially if you’re doing a one-time investment.

With SIPs, you don’t need to worry too much about daily NAV changes — because you invest regularly and get more units when prices are low.

When you decide to take your money back (called Redemption), the amount you get depends on the Current NAV.

Let’s say:

- You have 200 units of a fund.

- The current NAV is ₹70.

- So, your redemption value = 200 x ₹70 = ₹14,000.

That means, even if you invested when NAV was ₹50, what matters most is what it is today when you sell.

Personal Tip:

I once had to withdraw some money from a fund for an emergency. I checked the NAV on Kuvera app before redeeming. That helped me know exactly how much I’d get back.

Many people think a fund with a lower NAV (like ₹10) is better than one with a higher NAV (like ₹100). But that’s not true.

What really matters is how fast the NAV grows over time.

Let’s compare:

| Fund Name | Starting NAV | After 1 Year |

|---|---|---|

| Fund A | ₹10 | ₹12 (+20%) |

| Fund B | ₹100 | ₹120 (+20%) |

Both gave the same growth — 20%! So, a lower NAV doesn’t mean a better deal.

Always look at percentage returns, not just the number.

2. Using AUM for Your Research: What to Look For

AUM tells you how big a fund is and how many people trust it. Here’s how to use it wisely.

A. Fund Stability: Large AUM Can Indicate a Stable and Reputable Fund House

If a fund has a large AUM (Assets Under Management) — like thousands of crores — it usually means many investors trust it.

Examples:

- HDFC Equity Fund

- Axis Bluechip Fund

These funds are often managed by experienced teams and are less likely to shut down.

But remember — big size doesn’t always mean better returns.

B. Manager Expertise: Does a Big Fund Mean a Good Manager? (Not Always!)

Some large funds struggle to give good returns because they’re too big to move quickly.

Think of it like this:

- A small car can turn corners faster than a bus — no matter how experienced the driver is.

Similarly, a big fund may miss out on opportunities that smaller funds can grab.

So, don’t just pick a fund because it’s big. Check its performance history too.

C. Should You Worry About High or Low AUM? Finding the “Right” Size for Your Goals

Here’s a quick guide:

| AUM Size | Pros | Cons | Best For |

|---|---|---|---|

| High | Stable, trusted, good liquidity | May grow slowly | Risk-averse investors |

| Low | Can grow faster, flexible | Riskier, less popular | Goal-based investing, high-risk appetite |

Choose based on your goals and how much risk you’re comfortable with.

My Experience:

I once invested in a small fund with very low AUM. It gave great returns for two years, but later underperformed. I realized that while small funds can give good growth, they also come with more uncertainty.

Now that you understand NAV and AUM, here are other key things to look at before investing.

A. Expense Ratio: What You Pay the Fund House (e.g., AMFI Regulations on Fees)

All mutual funds charge a small fee called the Expense Ratio.

Expense Ratio includes:

- Fund manager fees

- Operating costs

- Marketing expenses

Even a small difference like 0.5% can reduce your returns over time.

Look for funds with a lower expense ratio, especially in index funds and ETFs.

You can find this info on platforms like Zerodha, INDMoney, Groww and Kuvera.

B. Fund Manager’s Track Record: How Have They Performed Consistently?

The person managing your fund makes a big difference.

Check:

- How long have they been managing the fund?

- How did the fund perform during their time?

You can find this information on the fund house website or apps like Zerodha.

C. Investment Objective: Does the Fund Match Your Financial Goals?

Don’t invest just because a fund is popular.

Ask yourself:

- Is this fund meant for long-term growth or short-term income?

- Does it match my goal — like buying a home, saving for retirement, or your child’s education?

For example:

- If your goal is 5 years away, a debt fund might be better than an equity fund.

D. Case Study: How Fund House Decisions May Be Influenced by AUM

Big funds with high AUM sometimes avoid risky but potentially rewarding investments — simply because they’re too big to act quickly.

Smaller funds can take more chances — which could lead to higher growth.

Let’s say:

- A small fund invests in a new tech company early.

- That company does well, and the fund grows fast.

But a large fund might not invest in that small company — because even if it does well, it won’t make a big difference to their overall AUM.

So, always consider fund size along with your own goals.

By now, you should feel confident using NAV and AUM to make smarter choices as an Indian investor. These are powerful tools — but they’re not the only ones. Combine them with expense ratio, fund objective, and track record to build a solid investment plan.

VII. Avoiding Common Mistakes – Learning from Others’ Experiences

1. Don’t Fall for These Traps: Understanding Common Pitfalls in India

Let’s talk about some of the most common mistakes Indian investors make when they start investing in mutual funds.

Some people think that a fund with a high NAV (Net Asset Value) is better — like how we might think an expensive phone is better than a cheaper one.

But this is not true for mutual funds.

What really matters is how much the NAV grows over time, not its current number.

Let’s look at two funds:

| Fund Name | Starting NAV | After 1 Year |

|---|---|---|

| Fund A | ₹10 | ₹15 (+50%) |

| Fund B | ₹100 | ₹110 (+10%) |

Even though Fund B has a higher NAV, Fund A gave you much better returns — 50% vs. just 10%.

So always look at percentage growth, not just the NAV number.

My Friend’s Story:

My friend once avoided a good fund because he thought its NAV was too high. Later, he saw it grew by 20% every year. Now he knows — focus on returns, not numbers.

B. Ignoring Performance for AUM: Focus on Consistent Returns, Not Just Fund Size

Just because a fund has a huge AUM (Assets Under Management) doesn’t mean it will give you good returns.

Big funds are often trusted and stable, but sometimes they grow too big to move quickly in the market.

Smaller funds can be more flexible and may grow faster.

So instead of picking a fund only because it’s popular or large, ask:

- Has it given consistent returns?

- Does it match your investment goal?

Always compare similar types of funds based on their past performance, not just AUM.

This is another mistake many new investors make.

In stocks, if a company’s share price goes up, it usually means the company is doing well.

But NAV is different.

It’s just the value of one unit of the fund. It doesn’t tell you if the fund is good or bad — it only tells you how much each unit costs today.

Think of it like this:

- If you buy milk at ₹60 per litre today and sell it at ₹65 tomorrow, you made a profit.

- But the price tag (₹60) isn’t what made you money — it was the change in price.

Same with NAV — it’s just a number. What matters is how fast it grows.

2. Thinking Long-Term: The Indian Investor’s Mindset for Success

Now that you know what not to do, let’s talk about what you should focus on.

A. The Power of Compounding: Letting Your Money Grow Over Time

One of the biggest advantages of investing in mutual funds is compounding — where your money earns money, and that money earns even more.

For example:

- If you invest ₹5,000 every month in a fund giving 12% annual returns, after 10 years, you’ll have around ₹11 lakh.

- After 20 years, it becomes ₹42 lakh!

That’s the power of staying invested and letting your money grow over time.

Market ups and downs are normal. So is seeing your NAV go down for a few days or weeks.

But if your goal is long-term — say, buying a house in 10 years or saving for retirement — short-term dips don’t matter much.

Here’s what to do:

- Keep investing regularly through SIPs.

- Don’t panic during small drops.

- Focus on long-term growth and consistency.

💡 My Experience:

In my early days of investment, I once panicked when my fund’s NAV dropped by 5% in a week. I thought of selling everything. But instead, I stayed calm and kept investing. In 6 months, the NAV not only recovered but went up by 18%! That taught me the importance of patience.

3. Where to Get Reliable Information and Avoid Scams in India

To avoid making mistakes and falling into traps, always get your information from trusted sources.

A. AMFI Website: Your Official Source for Mutual Fund Data and Education

The AMFI (Association of Mutual Funds in India) website — www.amfiindia.com — is a great place to start.

You can find:

- Updated NAV and AUM data

- Beginner-friendly guides

- Fund performance charts

- List of all registered mutual funds

It’s safe, official, and free to use.

B. SEBI’s Role: How Regulators Protect Your Money and Ensure Transparency in India

SEBI (Securities and Exchange Board of India) is the government body that watches over mutual funds and stock markets in India.

They ensure:

- Fair practices by fund houses

- Transparent reporting

- Protection of investor rights

If you face any issues with a fund or distributor, you can file a complaint on SEBI’s SCORES platform.

It’s easy to use and gives you a voice as an investor.

C. Reputable Financial News: Staying Updated and Informed (e.g., Economic Times, Livemint)

To stay updated on market trends, fund changes, and economic news, read trusted financial websites like:

- Economic Times

- Livemint

- Moneycontrol

- Financial Express

These sites give honest, verified updates without bias or hype.

Avoid relying on random WhatsApp forwards or unknown YouTube channels. Stick to reliable sources.

By avoiding these common mistakes and using trusted resources, you’re setting yourself up for success as an Indian mutual fund investor.

Remember:

Investing is not about being smart overnight — it’s about learning slowly, staying patient, and growing steadily over time.

VIII. Tools and Resources for Indian Mutual Fund Investors

Now that you understand the basics of NAV (Net Asset Value) and AUM (Assets Under Management), let’s look at the tools and resources available in India to help you invest smartly and track your investments with ease.

These tools are easy to use, many are free, and they can make your mutual fund journey smooth and stress-free.

1. Online Platforms Making Investing Easy (Specific Indian Examples)

You don’t need to visit a bank or broker to invest in mutual funds anymore. These apps make it simple and fast.

A. How to Open an Account and Invest Simply

With apps like Zerodha, INDMoney, Groww and Kuvera, you can:

- Open a mutual fund account from home in less than 10 minutes.

- Start investing with as little as ₹500.

- Choose from hundreds of funds based on your goals.

- Get free research reports and fund suggestions.

My Experience:

I opened my first mutual fund account using Kuvera during lockdown. I didn’t have to go anywhere — just upload my documents once and start investing right away.

These apps also give you clear updates on your portfolio every day.

B. MF Central: Your Go-To for Consolidated Portfolio View and Transactions

If you invest in mutual funds through different platforms, it can get confusing to track everything.

That’s where MF Central comes in.

It’s like a single dashboard for all your mutual fund investments, no matter where you bought them from.

With MF Central, you can:

- See all your investments in one place.

- Make transactions like SIPs or lump sum buys.

- Download consolidated reports easily.

This is especially useful if you’re investing across multiple apps like Zerodha, INDMoney, Groww and Kuvera.

Apps such as Zerodha, INDMoney, Groww and Kuvera are also great for staying updated on how your funds are doing every day.

They show you:

- The latest NAV of your funds.

- Changes in AUM over time.

- Performance charts and expert views.

- Alerts and notifications when something changes.

For example:

- If you invested in SBI Bluechip Fund, you can set a daily alert to know its new NAV.

- You can also see how its AUM has grown or fallen month after month.

All this helps you stay informed without spending hours digging through reports.

2. Tracking Your Investments: Staying on Top of Your Portfolio

Once you’ve started investing, it’s important to keep an eye on your money — but not too closely!

Here’s how to do it smartly:

Each mutual fund company (like HDFC Mutual Fund, ICICI Prudential, or Axis Mutual Fund) has its own website.

On these sites, you can:

- Log in to view your investment details.

- Check daily NAV updates.

- Download your monthly or quarterly account statements.

This is helpful if you want to dive deeper into a specific fund or review your transaction history.

B. Consolidated Account Statements (CAS): Your One-Stop Report from CAMS/KFintech

Every month, you’ll receive a Consolidated Account Statement (CAS) from either CAMS or KFintech — the two main registrars for mutual funds in India.

This report shows:

- All your mutual fund holdings in one PDF.

- Each fund’s current value.

- SIP dates and amounts.

- Any recent redemptions or switches.

Think of it like a bank statement for all your mutual fund investments.

Many apps allow you to set alerts so you never miss a change in your fund’s NAV.

For example:

- On ET Money, you can select a fund and tap “Set Alert” for NAV changes.

- On Groww, you can follow a fund and get notified when there’s a big shift.

This way, you can stay updated without checking manually every day.

3. Learning More: Resources for Continuous Growth and Investor Education

Learning doesn’t stop after your first investment. Here are some trusted sources to grow your knowledge along the way.

A. AMFI’s “Mutual Funds Sahi Hai” Campaign: Simple Explanations and Videos

The Association of Mutual Funds in India (AMFI) runs the popular campaign “Mutual Funds Sahi Hai”.

On their website amfiindia.com, you can find:

- Short videos explaining mutual funds in Hindi and English.

- Articles on topics like SIPs, NAV, and AUM.

- Tips for beginners and experienced investors alike.

It’s a great place to build your confidence step by step.

B. SEBI Portal for Investor Education: Understanding Your Rights

The Securities and Exchange Board of India (SEBI) protects your rights as an investor.

On their Investor education portal, you can:

- Learn about your rights as a mutual fund investor.

- Understand how to file complaints if something goes wrong.

- Read guides on avoiding frauds and fake schemes.

This is your safety net — always good to know what protections you have.

C. Financial Advisors: When to Seek Professional Help and Where to Find Registered Ones in India

Sometimes, you might want expert advice — and that’s okay!

If you’re unsure which fund to pick or how much to invest, you can talk to a registered financial advisor.

Some reliable platforms to find verified advisors include:

- Finserv MARKETS

- Scripbox

- PersonalFN

Make sure they are registered with SEBI or AMFI before sharing any personal details.

D. Monthly Factsheets and Their Benefits: Understanding Detailed Fund Reports

Every mutual fund publishes a monthly factsheet — kind of like a health report card for the fund.

These factsheets tell you:

- Which stocks or bonds the fund owns.

- Its performance over the last 3, 6, and 12 months.

- Expense ratio and fund manager comments.

- Risk levels and asset allocation.

You can usually find these on the fund house’s website under the “Downloads” or “Resources” section.

Tip:

I used to check the monthly factsheet of my fund to understand why it dipped one month. Turns out, it was because of market-wide losses, not poor fund management. That helped me avoid panic selling.

Using these tools and resources will help you stay informed, track your progress, and grow your wealth confidently.

Whether you’re investing ₹500 or ₹50,000, having the right tools makes all the difference. And remember — learning is part of the journey.

Keep exploring, stay curious, and let your money work for you!

Now that you understand NAV (Net Asset Value) and AUM (Assets Under Management), it’s time to take the next step.

These numbers are important, but they’re just the starting point. To make smarter investment decisions, you need to look at a few more things.

Let’s walk through what really matters when choosing a mutual fund in India.

Don’t stop at checking only NAV or AUM. These are like checking the price tag and popularity of a product — helpful, but not enough to know if it’s actually good for you.

Here’s what else to consider:

A. Always Look at Fund Objectives, Investment Strategy, and Underlying Holdings

Every mutual fund has a goal — some focus on growth, others on safety or regular income.

Ask yourself:

- Is this fund investing in safe assets like government bonds?

- Or is it going after high-growth stocks?

You can find this info in the fund’s factsheet or on platforms like Groww or AMFI website.

For example:

- If your goal is to save for your child’s education in 5 years, a debt fund might be better than an equity fund.

- But if you’re saving for retirement 20 years away, a well-managed equity fund could give better returns.

So always match the fund’s strategy with your own goals.

Think of a fund manager like the driver of a car — even the best car won’t reach its destination quickly if the driver doesn’t know the route.

A good fund manager knows how to:

- Pick the right stocks

- Avoid big losses during market falls

- Deliver consistent returns over time

Check how long the current fund manager has been handling the fund and how it performed under them.

My Experience:

I once invested in a fund because its NAV was growing fast. Later, I found out the fund manager had changed, and performance dropped the next year. Since then, I always check who’s managing the fund before investing.

C. Compare 2-3 Similar Funds: Don’t Just Pick the First One You See

It’s easy to pick the first fund that shows up in search results — but don’t rush.

Take time to compare 2–3 similar funds based on:

- Past returns (over 3, 5, or 10 years)

- Risk level

- Consistency

- Expense ratio

Most apps like Zerodha, INDMoney, Groww and Kuvera let you compare funds.

This helps you avoid making a decision based on just one number like NAV or AUM.

To get a full picture of a fund, here are other key numbers to check:

A. Expense Ratio: Keep an Eye on the Costs

Every mutual fund charges a small fee for managing your money — called the Expense Ratio.

Even a small difference like 0.5% can affect your returns over time.

Look for funds with lower expense ratios, especially in index funds and ETFs.

Example:

- Fund A has a 1.0% expense ratio.

- Fund B has a 0.6% expense ratio.

Over 10 years, Fund B could leave you with more money — even if both give similar returns.

B. Portfolio Turnover Ratio: How Often the Fund Buys/Sells

This tells you how often the fund buys and sells stocks.

High turnover means more trading → which leads to higher costs → which affects your returns.

Low turnover is usually better unless the fund is actively trying to catch quick market moves.

C. Past Returns (Over 3, 5, 10 Years): Look for Consistency, Not Just Recent Hype

A fund that gave 30% returns last year may have given -10% the year before.

That’s not consistent.

Instead, look for funds that give steady returns over time — say around 12–15% every year.

Consistency beats short-term hype.

D. Risk-Adjusted Returns: Understanding Returns vs. Risk Taken

Some funds give high returns — but only by taking big risks. Others give moderate returns with less risk.

Use metrics like Sharpe Ratio to see how much return a fund gives per unit of risk.

A higher Sharpe Ratio = better returns for the same amount of risk.

You can find this in the fund’s monthly factsheet or on financial platforms like Morningstar or Value Research.

3. When and Where to Ask for Help or File Complaints in India

If you ever feel confused or face issues with your investments, help is available.

Here’s where to go:

A. Using a Registered Mutual Fund Distributor or Financial Planner

Sometimes, you may want expert advice — and that’s okay!

But always use:

- SEBI-registered advisors

- AMFI-certified distributors

These professionals follow rules and offer reliable guidance.

You can find them on platforms like:

- Finserv MARKETS

- Scripbox

- PersonalFN

Always ask for their registration number before sharing any personal details.

B. Where to File Complaints: The SEBI SCORES Platform for Investor Grievances

If something goes wrong — like delays in processing your SIP, incorrect NAV, or misleading advice — you can file a complaint with SEBI using the SCORES platform

Steps:

- Register on the site.

- Select “Investor Grievance.”

- Fill in your details and upload proof.

- Submit — and track your case online.

This is a free service provided by SEBI to protect your rights as an investor.

Tip from My Friend:

A friend of mine faced a delay in his redemption. He filed a complaint on SCORES, and within a week, the issue was resolved. It’s a simple process and works well.

By now, you should know that NAV and AUM are just the beginning.

To invest wisely, always dig deeper — understand the fund’s goals, check the manager’s record, and compare options.

And remember — there’s no shame in asking for help or raising a concern if something feels off. Investing is a journey, and you’re not alone!

X. Conclusion – Your Path to Financial Confidence with Mutual Funds

1. You’ve Got This: Taking Your First Steps in Mutual Fund Investing

You’ve come a long way — and now you understand two of the most important terms in mutual funds: NAV (Net Asset Value) and AUM (Assets Under Management).

Let’s quickly recap:

- NAV is like the price tag of your fund. It tells you how much each unit is worth today.

- AUM is the total money invested in the entire fund — like the size of the money pool you’re part of.

They’re both useful, but they tell you different things.

B. The Power of Knowledge: Making Informed Choices Leads to Better Outcomes

Now that you know what these numbers mean, you’re no longer investing blindly.

You can:

- Understand where your money is going

- Track your growth daily

- Make better choices when picking a fund

And that makes all the difference between guessing and growing wisely.

2. Building Wealth, One Step at a Time: Your Financial Future is in Your Hands

Mutual funds are not just for rich people or experts. They’re for you — whether you’re saving for a home, your child’s education, or retirement.

A. Long-Term Benefits: How Mutual Funds Can Help You Achieve Goals Like Retirement, Home Purchase, or Child’s Education

Here’s the secret to success:

Start small, stay regular, and give your money time to grow.

Even ₹500 every month through a SIP (Systematic Investment Plan) can become a big amount over 10–20 years thanks to compounding.

Think of it like planting a tree:

- You don’t see results in the first few months.

- But after a few years, it grows tall and gives fruit.

Your investments work the same way.

B. Continuous Learning: Stay Curious, Stay Informed, and Keep Growing Your Wealth

The more you learn, the better you’ll get at managing your money.

Don’t stop here. Keep reading, ask questions, and explore new ways to improve your investment decisions.

There’s always something new happening in the market — and staying updated helps you make smarter moves.

3. Remember: Mutual Funds Truly Sahi Hai – But Stay Smart!

Yes, mutual funds are a great way to grow your money — but only if you invest wisely.

Many beginners get stuck trying to predict future NAV or worry too much about AUM.

But remember:

- NAV doesn’t predict returns — it just shows today’s value.

- AUM doesn’t guarantee performance — it just shows how big the fund is.

Use them as tools, not decision-makers.

B. Take Action with the Knowledge You’ve Gained: Start Your SIP or Lump Sum Investment

Now that you have clarity, take the next step.

Open an account on platforms like:

Choose a fund that matches your goal and start investing — even with a small amount.

My Experience:

I was once confused like you — unsure where to begin. Then I started with ₹1,000 in a simple index fund on INDMoney. Today, that small investment has grown steadily over time. All because I took action early.

C. Investing is a Journey, Not a Race: Be Patient and Consistent

Investing isn’t about getting rich overnight. It’s about building wealth slowly and steadily.

So:

- Don’t panic during short-term dips.

- Don’t chase quick profits.

- Focus on your goals and keep investing regularly.

If you stay patient and consistent, mutual funds will help you build a stronger financial future — one rupee at a time.

Start small, stay smart, and let your money work for you.

Happy investing! 🚀

NAV is the price of one unit of a mutual fund.

AUM is the total money invested in the entire fund.

No. A higher NAV doesn't mean better returns or a more expensive fund. What matters is how much it grows over time.

NAV is updated **daily** and published by 9 PM on most platforms.

You can check them on:

- Fund house websites

- AMFI website

- Apps like Groww, Zerodha Coin, ET Money

5. What is considered a good AUM for a mutual fund?

There's no fixed number. AUM should be balanced — not too small (to ensure credibility) and not too large (to maintain agility).

6. Can a fund's AUM decrease? If yes, what are the common reasons?

Yes. AUM can fall due to:

- Poor performance

- Investors withdrawing money

- Market declines

7. Is it generally safe to invest in a fund with a very low AUM?

It depends. Very small AUM funds can be riskier but may offer high growth. Always check the fund's performance and manager.

8. How does a fund's AUM size indirectly affect my investment returns?

Larger AUM can reduce expense ratios but may slow down the fund's ability to adapt. Smaller AUM allows flexibility but may lack resources.

No. NAV alone doesn't determine returns. Look at past performance, fund objective, and risk profile.

SEBI mandates regular audits and disclosures. Any discrepancies can be reported via the SCORES portal.