Table of Contents

- I. Understanding the Basics of Personal Finance

- II. Why Personal Finance Is Important

- III. Core Principles of Personal Finance

- IV. Practical Steps to Manage Your Personal Finances

- V. Common Mistakes to Avoid

- VI. Tools, Apps, and Resources in India

- VII. The Future of Personal Finance in India – Trends to Watch

- VIII. Conclusion

- IX. Frequently Asked Questions (FAQs)

- 1. Can I manage my finances without any professional help?

- 2. How do I start if I earn very little?

- 3. What should I do if I already have debt?

- 4. Should I invest in gold or real estate?

- 5. Is it okay to borrow from family or friends?

- 6. How do I know if I'm spending too much?

- 7. Can I start investing before marriage or having kids?

- 8. How much should I save each month?

- 9. Do I really need insurance?

- 10. How can I teach my kids about money?

Let’s talk about something most of us deal with every day — money. More specifically, how to manage it well, so you can sleep better at night and plan for the future without stress.

You’re probably here because you’ve wondered:

“What is personal finance?”

“How does it affect me as an Indian?”

“Why should I even care?”

This article will help you understand what personal finance really means, why it matters in India today, and how it can change your life — no matter how much or how little you earn. We’ll also cover some core principles that are easy to follow, with real-life examples from our own culture and daily struggles.

So let’s get started!

I. Understanding the Basics of Personal Finance

1. What is Personal Finance?

A. Definition in simple terms

Personal finance is basically how you manage your money as an individual. That includes things like:

- How much you earn (salary, side income, etc.)

- How much you spend (rent, food, bills)

- How much you save

- And how wisely you invest

It’s not about becoming a millionaire overnight. It’s more like making sure you have enough for things that matter to you — whether it’s buying a new phone, saving up for your sister’s wedding, or just not stressing about next month’s rent.

B. Why it matters even if you’re not rich

A lot of people think personal finance is only for those who earn big. But that’s not true. Even if you make Rs. 10,000 or Rs. 50,000 a month, having a system helps you:

- Avoid stress around money

- Save for important goals like buying a phone, paying school fees, or going on a family trip, etc.

- Handle emergencies without borrowing from relatives or friends — like when your bike breaks down or your mobile stops working

- Sleep better knowing you’re prepared for whatever comes next

I remember a time when my friend used to spend his salary within 15 days — on eating out, shopping, and even small gifts. Then one month, his 2-wheeler needed a major repair, and he had zero backup. He had to borrow from me. That was the moment I realized: personal finance isn’t optional — it’s essential.

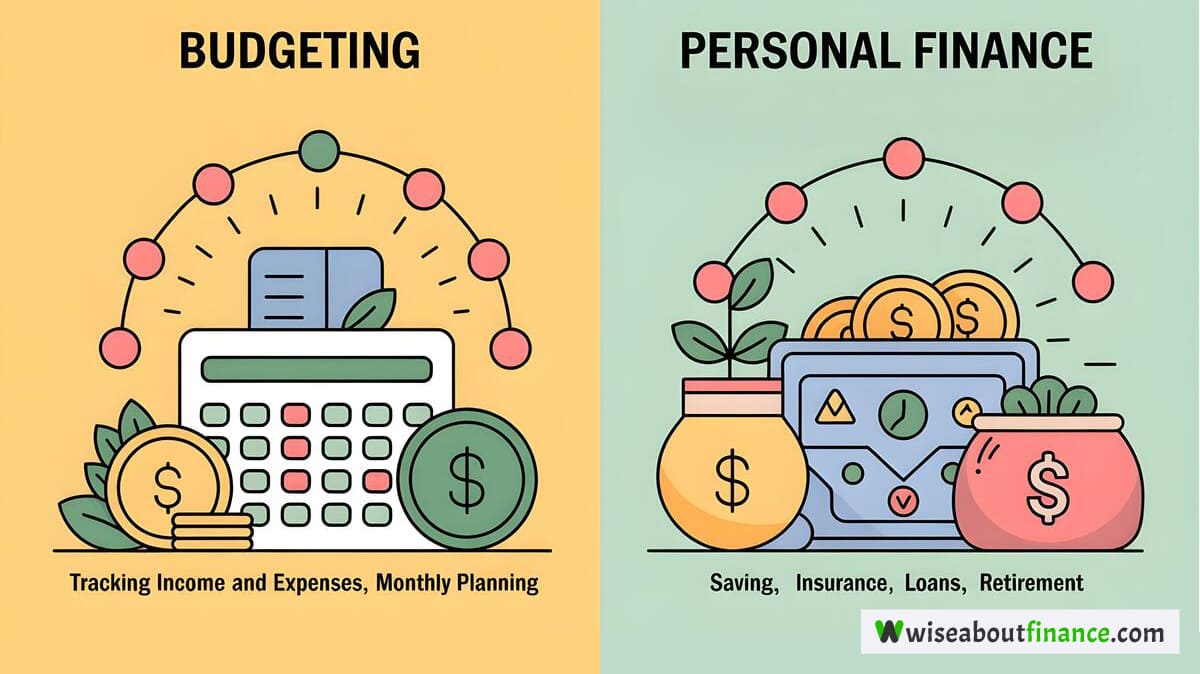

C. How personal finance differs from household budgeting

Budgeting is part of personal finance, but they aren’t the same thing.

Think of it like this:

- Budgeting = tracking where your money goes each month (like groceries, school fees, etc.)

- Personal finance = covers budgeting + savings, investments, insurance, loans, retirement planning, and more

Imagine you run a small tea stall. Budgeting would be keeping track of your daily sales and expenses. Personal finance would be thinking ahead — saving for a bigger space, insuring your stock, maybe even investing in a second location someday.

Here’s a quick example:

Say you earn Rs. 20,000 per month. Your monthly expenses look like this:

- Rent – Rs. 4,000

- Food – Rs. 3,500

- Travel – Rs. 1,000

- Mobile & Electricity – Rs. 1,000

- Other stuff – Rs. 3,000

That’s Rs. 12,500 total.

If you don’t track your remaining Rs. 7,500, chances are it disappears quickly. But with basic personal finance:

- Save Rs. 2,000 for emergencies

- Invest Rs. 1,000 in mutual funds or FDs

- Keep Rs. 2,500 for unexpected costs

- Spend Rs. 2,000 on fun stuff guilt-free

Suddenly, you’re not just surviving — you’re building something solid.

2. The Indian Context: Why It Matters Here

A. Rising cost of living and inflation in India

Inflation is hitting hard these days.

Prices of onions, petrol, vegetables, and even mobile data keep going up. What used to cost Rs. 100 last year now costs Rs. 120.

If we don’t manage our money smartly, we end up spending more than we earn — and fall into debt.

B. Cultural mindset around money

Many families in India still believe that “discussing money is rude.” But the truth is, not talking about money leads to poor decisions — like taking expensive loans without understanding interest rates, or buying gold without checking where it fits in your investment plan.

We need to shift that mindset. Talking about money isn’t shameful — it’s practical.

C. Financial independence at every life stage

Whether you’re fresh out of college, married with kids, or nearing retirement — personal finance helps you stay independent.

For example, a young person might use it to build an emergency fund before moving to a new city for work. A parent might plan for their child’s education. Someone older might start thinking about retirement savings.

Each stage of life has its own needs — and personal finance adapts to all of them.

D. Role of banks, regulators (RBI), and digital platforms

Today, thanks to the Reserve Bank of India (RBI) and platforms like Paytm, PhonePe, and Google Pay, it’s easier than ever to manage your money.

You can:

- Open a bank account online

- Start investing in mutual funds with just Rs. 500

- Track your credit score for free

- Get health insurance in minutes

These tools make financial planning accessible to everyone — even those who thought it wasn’t for them.

II. Why Personal Finance Is Important

1. Achieving Life Goals

A. Buying a home

Owning a house is a dream for many Indians. But unless you win the lottery, it takes years of disciplined saving and planning.

With good personal finance habits, you can set aside money regularly, choose the right loan options, and avoid unnecessary debt.

B. Funding education

Education is expensive, especially if you or your kids want to study abroad or join a top engineering or medical college.

By starting early and investing wisely, you can build a fund without stressing over tuition fees.

C. Retiring with dignity

Retirement might feel far away, but time flies. If you start saving early — say, in PPF or NPS — you can enjoy your golden years without depending on others financially.

You too can start small! Begin investing just Rs. 1,000/month in a mutual fund at age 25. Imagine turning that consistent, modest investment into over Rs. 10 lakhs by age 60!

2. Reducing Stress and Improving Mental Health

A. Link between money problems and anxiety

Money worries are one of the biggest causes of stress in India today. People lose sleep over EMIs, job loss, or sudden hospital bills.

But when you have a clear plan — like an emergency fund, a monthly budget, and some investments — it gives you peace of mind.

B. How planning helps reduce uncertainty

When you know exactly how much you earn, how much you spend, and how much you save — you feel in control. You stop worrying about surprises because you’re ready for them.

One of my cousins used to panic whenever his car broke down. He’d have to take a loan or borrow from family. Then he started saving Rs. 2,000/month in a separate fund for emergencies. Now, he handles repairs calmly — and even uses the money for travel sometimes!

3. Protecting Against Emergencies

A. Medical emergencies

Health issues can strike anytime. And hospital bills? They can drain your savings fast. Having health insurance and an emergency fund is a must.

B. Job loss or income disruption

With layoffs happening across industries, having a backup plan is crucial. Ideally, you should have 3–6 months’ worth of expenses saved up — so you can survive even if you lose your job.

C. Natural disasters or pandemics

The pandemic taught us a harsh lesson — life can change overnight. Those who had emergency funds or insurance fared much better than those who didn’t.

My distant uncle runs a small shop. When lockdown hit, his income dropped almost completely. But since he had been saving a little every month, he managed to keep his business alive and support his family without borrowing.

III. Core Principles of Personal Finance

1. Income Management – Earning Smartly

A. Know all your sources of income

Your main salary isn’t the only way to earn. Side gigs like freelancing, teaching, or selling homemade products online can add extra income.

B. Understand tax deductions and net salary

Know how much you actually take home after taxes. This helps you plan your expenses better and avoid surprises during tax season.

C. Explore side income opportunities in India

India has a booming gig economy. Platforms like Swiggy, UrbanClap, and Fiverr offer flexible earning options. Even students can do micro-jobs online.

D. Grow your income through upskilling and promotions

Invest in learning new skills — like digital marketing, coding, or spoken English. These open doors to better jobs and higher pay.

2. Expense Management – Spending Wisely

A. Differentiate between needs and wants

Needs are things you can’t live without — food, rent, medicine. Wants are things that improve life — like dining out or a new smartphone. Learn to prioritize needs first.

B. Use budgeting tools to track daily expenses

Apps like Mint, Walnut, or even Excel sheets help you track where your money goes — so you can cut back on unnecessary spending.

C. Avoid lifestyle inflation and impulse buying

Just because you got a raise doesn’t mean you should upgrade your phone or move to a pricier flat. Keep your lifestyle stable and let the extra money go toward savings or investments.

D. Reduce unnecessary recurring payments

Check your mobile apps, OTT subscriptions, and other auto-debits. Cancel ones you don’t use — you’ll be surprised how much you save each month.

3. Budgeting: Living Within Your Means

A. 50-30-20 rule explained

This rule divides your income into:

- 50% for needs

- 30% for wants

- 20% for savings and investments

It’s a simple way to stay balanced.

B. Creating a realistic monthly budget

Start by listing your income and fixed expenses. Then allocate money for variable costs like groceries and transport. Finally, decide how much you can save.

C. Adjusting budgets based on life changes

If you get married, have a baby, or change jobs — your budget should change too. Stay flexible and keep updating your plan.

4. Saving Before Spending

A. Automate savings

Set up automatic transfers to your savings account or mutual fund. That way, you save first — before you even see the money.

B. Treat savings as a fixed expense

Like paying rent or electricity bill, treat savings as a non-negotiable part of your monthly plan.

C. The power of compounding

Even small amounts grow over time. For example, if you invest Rs. 1,000/month at 12% returns, in 20 years, you’ll have over Rs. 10 lakhs — without doing anything else.

5. Investing for Growth

A. Difference between saving and investing

Saving keeps your money safe but doesn’t grow much. Investing grows your money over time — though it comes with some risk.

B. Risk vs reward – understanding your comfort zone

Some people prefer fixed deposits (low risk, low return). Others go for mutual funds or stocks (higher risk, higher potential gain). Choose what suits you.

C. Investment options in India

Popular choices include:

- Fixed Deposits (FD)

- Public Provident Fund (PPF)

- National Pension Scheme (NPS)

- Mutual Funds

- Gold ETFs

All are easy to start with small amounts.

D. Diversification – don’t put all eggs in one basket

Spread your investments across different types — like a mix of FDs, mutual funds, and maybe even some gold. That way, if one dips, the others balance it out.

6. Managing Debts Wisely

A. Good debt vs bad debt

Good debt helps you grow — like a home loan or education loan. Bad debt is high-interest borrowing like credit card dues or personal loans.

B. Strategies to reduce debt

Pay off high-interest debts first. Avoid using credit cards for everyday expenses. Make a repayment plan and stick to it.

C. Understanding credit scores and their importance in India

Your credit score affects whether you get approved for loans. Check it regularly (CIBIL offers free checks once a year), and try to keep it above 750.

7. Insurance – Protecting Against the Unexpected

A. Health, term, life, and vehicle insurance

These protect you and your family from big losses. For example, a health insurance policy can save you from paying huge hospital bills.

B. Choosing the right coverage

Don’t just buy the cheapest plan. Read the fine print and pick coverage that matches your needs.

C. Common mistakes while buying insurance

People often under-insure or buy policies they don’t fully understand. Always compare plans and ask questions before signing up.

IV. Practical Steps to Manage Your Personal Finances

1. Start with Goal Setting

A. Short-term goals (0–2 years)

These are things you want to achieve soon — like saving for a new laptop, a vacation, or paying off a small loan.

Start by setting a clear target: “I want to save Rs. 20,000 in 6 months.” Then divide it into smaller chunks — Rs. 3,500/month — and stick to it.

B. Medium-term goals (3–5 years)

This could be buying a car, saving for a down payment on a house, or building a small business fund.

For example, if you want to buy a used car worth Rs. 4 lakh in 3 years, aim to save around Rs. 11,000 every month.

C. Long-term goals (5+ years)

Think retirement planning, children’s education, or even starting your own company.

Even if these feel far away, start small. Investing Rs. 2,000/month in PPF or mutual funds today will grow significantly over time.

A friend of mine started investing Rs. 3,000/month in a SIP when she was 25. By 40, she had over Rs. 12 lakhs — just by staying consistent.

2. Build an Emergency Fund

A. Ideal size – 3–6 months’ worth of expenses

Your emergency fund should cover basic needs like rent, food, medical bills, and transport — for at least 3–6 months.

If you spend Rs. 15,000 a month, aim to save between Rs. 45,000 and Rs. 90,000 as backup.

B. Where to keep it – liquid funds or savings account

Keep this money easily accessible. You can use:

- High-interest savings accounts (like Kotak or RBL)

- Liquid mutual funds (like those on Groww or Zerodha Coin)

Avoid locking it up in fixed deposits or investments that can’t be withdrawn quickly.

C. Replenish after use

If you use some of your emergency fund — say, for a medical expense — rebuild it slowly. Set aside a small amount each month until it’s back to full strength.

3. Create a Monthly Budget

A. List all income sources

Include your salary, side income, rental income — everything you earn.

Write it down clearly so you know exactly how much you have to work with.

B. Categorize and track expenses

Divide your spending into:

- Needs: Rent, groceries, utilities, EMIs

- Wants: Eating out, subscriptions, shopping

- Savings & Investments: FDs, SIPs, etc.

Use apps like ET Money or Mint to track where your money goes.

C. Identify areas to cut costs

You might realize you’re spending too much on OTT subscriptions or eating out.

Cutting just two restaurant meals a month can save you Rs. 1,000+ — which can go into your emergency fund or investments.

4. Choose the Right Tools

A. Mobile apps for budgeting in India

Here are a few popular ones:

- Zerodha Coin & Groww: Great for investing in mutual funds

- Paytm Money: Easy interface, great for beginners

- ET Money: Tracks spending, helps build budgets

Pick one that suits your style and stick with it.

B. Spreadsheets and notebooks

Not everyone loves apps. Some prefer writing things down. Use Excel sheets or Google Sheets — they’re free and easy to update.

Or try a simple notebook to jot down daily expenses.

C. Online calculators

Websites like BankBazaar or HDFC offer useful tools like:

- Loan EMI calculators

- Retirement planners

- SIP return estimators

They help you plan better without guesswork.

5. Invest Smartly

A. Learn about investment options

Don’t jump into anything blindly. Understand what you’re investing in:

- Fixed Deposits = safe but low returns

- Mutual Funds = medium risk, better returns

- Gold ETFs = good for diversification

- PPF = tax-free long-term growth

Start with basics before exploring more complex options.

B. Open a Demat and Trading Account (if needed)

If you want to invest in stocks, open a Demat account with brokers like Zerodha or INDmoney.

But remember: stock markets can be risky. Don’t invest more than you can afford to lose.

C. Start small with SIPs in mutual funds or PPF

Systematic Investment Plans (SIPs) allow you to invest small amounts regularly — like Rs. 500/month.

PPF offers safety and tax benefits — perfect for long-term goals.

One of my friends started with Rs. 1,000/month in a SIP. In 7 years, he had over Rs. 1 lakh — no big effort, just consistency.

V. Common Mistakes to Avoid

1. Not having a clear financial plan

A. Jumping into investments without goals

Many people invest because their friend did — not because they have a goal. This leads to panic selling when the market dips.

Always ask: What am I investing for?

B. Ignoring insurance or emergency funds

Some think investing is enough. But without insurance or an emergency fund, one hospital bill can undo months of hard work.

Cover yourself first — then grow your money.

2. Overspending on wants

A. Lifestyle inflation after salary hikes

Getting a raise feels great — but don’t upgrade your lifestyle immediately. Keep your old habits and invest the extra money.

B. Peer pressure to buy expensive gadgets or cars

Just because others are buying the latest phone or SUV doesn’t mean you should too. Focus on what you need, not what others expect.

3. Poor debt management

A. Using credit cards for daily expenses

Credit cards are convenient, but using them for daily purchases often leads to high-interest debt.

Only use them if you can pay the full bill every month.

B. Borrowing from friends/family without repayment plans

It’s okay to borrow — but only if both sides agree on when and how it will be repaid. Otherwise, it damages relationships.

4. Following trends blindly

A. Investing in crypto or penny stocks without research

Crypto and penny stocks can give big returns — but also carry huge risks. Don’t invest unless you understand what you’re getting into.

YouTube videos and WhatsApp forwards aren’t always reliable. Always consult a certified advisor or do your own research before investing.

5. Procrastination

A. Delaying retirement planning until late 40s

Retirement may seem far away, but the earlier you start, the easier it becomes. Even Rs. 500/month adds up over 30 years.

B. Waiting for “perfect” time to start

There’s no perfect time. The best time to start is now. Every rupee saved today works harder tomorrow.

VI. Tools, Apps, and Resources in India

1. Popular Personal Finance Apps

A. Zerodha Coin

Ideal for investing in gold, ETFs, and mutual funds.

B. Groww

Simple interface, excellent for beginners.

C. Paytm Money

Great for tracking expenses and investing in mutual funds.

D. ET Money

User-friendly and helps set financial goals.

2. Government Schemes Worth Knowing

A. Pradhan Mantri Jan Dhan Yojana (PMJDY)

Allows anyone to open a zero-balance bank account with insurance coverage.

B. Atal Pension Yojana (APY)

Provides monthly pension after retirement — ideal for self-employed and unorganized workers.

C. Sukanya Samriddhi Yojana (SSY)

Excellent for parents saving for a girl child’s future — offers high interest and tax benefits.

D. National Pension System (NPS)

A government-backed pension scheme that allows flexible investments and tax deductions.

3. Books and YouTube Channels

A. Books: What Smart Indians Do With Their Money

A must-read for understanding Indian financial habits and smart strategies.

B. YouTube: Pushkar Raj Thakur, Arthgyaan

These creators explain complex topics in simple Hindi/English — very helpful for visual learners.

4. Websites and Blogs

A. Economic Times Personal Finance

Offers expert advice and news updates.

B. Mint Lounge

Focuses on personal finance and lifestyle.

C. Value Research Online

Trusted source for mutual fund reviews and ratings.

D. Personal finance blogs by experts

Follow blogs like Arthgyaan, The Financial Literate, or MyMoneyGoal for insights tailored to India.

VII. The Future of Personal Finance in India – Trends to Watch

1. Rise of Fintech and Digital Banking

More people are using apps to bank, invest, and insure themselves. UPI, mobile wallets, and digital loans are becoming mainstream.

2. Increasing awareness and financial literacy

Thanks to YouTube, podcasts, and online courses, more Indians are learning how to manage money wisely.

3. Evolving investment landscape

New options like direct mutual funds, ETFs, and fractional shares are making investing easier and cheaper.

4. Impact of economic growth on personal finance

As India grows, job opportunities increase and salaries rise — giving us more power to build wealth if we manage our money well.

VIII. Conclusion

Good habits today — like saving, budgeting, and investing — lead to freedom tomorrow. You’ll sleep better, worry less, and live life on your terms.

Progress takes time. Don’t expect overnight results. Just keep showing up, saving a little, and learning along the way.

Start with a small goal. Make a budget. Open a SIP. Track your expenses. These tiny actions create massive change.

You don’t need to be rich to start managing your money. You just need to start.

So go ahead. Take that first step. Because the sooner you begin, the more time your money has to grow — and the closer you’ll be to the life you deserve.

Your financial journey starts today! 💪

IX. Frequently Asked Questions (FAQs)

1. Can I manage my finances without any professional help?

Yes! Most people learn through apps, books, and YouTube. Only consult a professional if your situation is complex.

2. How do I start if I earn very little?

Start small — save even ₹100 per month. Consistency builds wealth faster than you think.

3. What should I do if I already have debt?

Prioritize high-interest debts first. Consider balance transfer options or consolidating loans.

4. Should I invest in gold or real estate?

Gold is good for diversification. Real estate requires large capital. Both can be part of a balanced portfolio.

5. Is it okay to borrow from family or friends?

Only if there's a clear agreement and both parties agree on repayment.

6. How do I know if I'm spending too much?

Track your expenses. If your needs take less than 50% of your income, you're on track.

7. Can I start investing before marriage or having kids?

Absolutely! Early investing gives you more time to grow your money.

8. How much should I save each month?

Aim for at least 20% of your income. Even 10% is a great start.

9. Do I really need insurance?

Yes, especially health and term insurance. They protect your family from sudden financial shocks.

10. How can I teach my kids about money?

Give them a piggy bank, explain savings, and involve them in small budgeting decisions.