Table of Contents

- I. Welcome to Investing: Why Mutual Funds Make Sense for You

- II. The Big Wins: Why Mutual Funds Stand Out for Indian Beginners

- 1. Professional Money Managers Work for You

- 2. Spreading Out Your Risk (Diversification)

- 3. Start Small, Grow Big (Affordability and SIPs)

- 4. The Magic of Compounding: Your Money’s Best Friend

- 5. Easy to Buy and Sell (Liquidity)

- 6. Clear and Simple Rules (Transparency & Regulation by SEBI)

- 7. Tax Benefits (Where Applicable)

- 8. Summary of This Section

- III. Getting Started: Key Terms Every Indian Beginner Should Know

- IV. Finding Your Fit: Types of Mutual Funds for Indian Beginners

- V. Your First Steps: How to Invest in Mutual Funds in India

- 1. Step 1: Figure Out Your Goals (Why Are You Investing?)

- 2. Step 2: Know Your Risk Comfort Zone

- 3. Step 3: Pick the Right Fund for You

- 4. Step 4: Complete Your KYC (Know Your Customer) – It’s Mandatory!

- 5. Step 5: Choose Your Investment Platform (Online vs. Offline)

- 6. Step 6: Start Your SIP (or Lump Sum)

- 7. Step 7: Keep an Eye on Your Investment

- 8. Summary of This Section

- VI. Investing Smart: Important Checks & Avoiding Common Mistakes

- 1. Important Checks for Proactive Investing

- 2. Common Mistakes Indian Beginners Must Avoid

- A. Waiting Too Long to Start Investing

- B. Stopping SIPs During Market Ups and Downs (Panic Selling)

- C. Investing Without a Clear Goal or Plan

- D. Not Doing Your Homework (Research Beyond Tips)

- E. Chasing Only Past Returns (Focus on Consistency Instead)

- F. Falling for “Get Rich Quick” Schemes

- G. Ignoring Your Nominee Details and Other Formalities

- 3. Summary of This Section

- VII. Real-Life Investment Journeys for Indian Beginners

- VIII. Helpful Friends: Tools and Resources for Indian Investors

- IX. Growing Your Wealth: Beyond the Basics & India’s Investment Future

- X. Conclusion – Your Investment Journey Starts Now!

- XI. Frequently Asked Questions (FAQ) About Why Mutual Funds Are Ideal For Beginners In India?

- 1. Is it safe to invest in mutual funds in India?

- 2. How much money do I need to start investing in mutual funds?

- 3. Can I lose money in mutual funds?

- 4. What is the difference between a direct fund and a regular fund?

- 5. How do I choose the best mutual fund?

- 6. What is KYC and why is it important for mutual funds?

- 7. How are mutual fund returns taxed in India?

- 8. Can I stop my SIP anytime?

- 9. What is the role of AMFI and SEBI?

- 10. Should I invest in mutual funds or Fixed Deposits (FDs)/PPF?

If you’re new to investing and wondering where to begin, mutual funds might be the perfect place to start. Why mutual funds are ideal for beginners is a question many Indians ask themselves before stepping into the world of finance.

The truth is, you don’t need a large sum of money or expert knowledge to invest — just the willingness to take small, consistent steps toward your financial goals.

In this article, we’ll walk you through everything you need to know about mutual funds in India:

- What they are

- How they work

- Why they’re great for beginners

- How to get started

- Common mistakes to avoid

- Real-life examples

- Tools that can help

Let’s dive in and start building your investment journey today!

I. Welcome to Investing: Why Mutual Funds Make Sense for You

1. Feeling Nervous About Investing? You’re Not Alone!

A. The Common Doubts of a New Investor in India

It’s completely normal to feel unsure when you hear words like “stocks”, “markets”, or “investment.”

Many people think:

- What if I lose my money?

- Do I need a lot of money to start?

- How do I even begin?

But here’s the truth: You don’t have to be an expert to invest.

In fact, mutual funds are designed specifically to make investing easy and safe for people who are just starting out.

It’s okay to feel unsure. Most successful investors once felt the same way — and they started with small steps too.

For example:

Let’s say you’re thinking about investing but feel confused by all the jargon. That’s totally normal! Just like when you first learned how to use your smartphone — it seemed complicated at first, but now it’s second nature. Investing works the same way. Start small, take one step at a time, and soon you’ll feel more confident.

B. Why Investing Early, Even Small Amounts, Matters

Time is one of your biggest friends when it comes to growing money. Even if you start with as little as ₹500 or ₹1,000 per month, the power of compounding can turn those small amounts into big savings over time.

For example:

- If you invest ₹1,000 every month starting at age 25, and earn a 12% return each year, by age 60, you could have over ₹40 lakhs.

- But if you wait until age 35 to start, you’d only end up with around ₹15 lakhs.

That’s the magic of starting early.

Starting small but starting early can lead to big results over time thanks to compounding.

For example:

Think of it like planting a tree. If you plant a mango tree today, you won’t get fruit immediately. But if you water it regularly and give it time, after a few years, you’ll enjoy fresh mangoes every season. Similarly, investing small amounts early gives your money time to grow and multiply.

2. What Exactly is a Mutual Fund? (Think “Investment Potluck”)

A. How Many Small Investments Come Together

Imagine a group of friends pooling money together to buy snacks for a party. Each person contributes a small amount, and everyone gets to enjoy a variety of food.

A mutual fund works the same way.

- Hundreds or thousands of investors put their money together.

- That pooled money is then invested in stocks, bonds, or other assets.

- A professional fund manager decides where to invest the money.

This means you get access to a wide range of investments without needing a huge amount of money.

Mutual funds let many small investors pool their money so they can all benefit from diversified investments.

For example:

Let’s say you want to eat pizza, burgers, and fries at a party, but you can only afford one item. If you team up with two friends and each of you buys one dish, now you can all enjoy everything.

That’s exactly how mutual funds work — many people chip in a little money, and together they get access to a variety of investments.

B. The Idea of a Professional Managing Your Money

You don’t need to track stock prices daily or worry about picking the right company. Instead, you leave that job to a fund manager — someone who has experience and knowledge in investing.

They decide which companies to invest in, how much to invest, and when to sell. This makes life easier for you, especially if you’re just starting out.

With mutual funds, professionals manage your money so you don’t have to stress about market details.

For example:

Say you’re planning a birthday party and want to choose the best venue, menu, and decorations. Would you rather plan everything yourself or hire a professional event planner who does this every day? Probably the latter.

Similarly, a mutual fund manager plans your investments so you don’t have to spend hours researching stocks or tracking markets.

3. Why Mutual Funds are a Great Starting Point for Indians

A. Simplicity and Accessibility for First-Timers

One of the best things about mutual funds is that they are simple to understand and easy to invest in.

You don’t need to open a demat account or learn complex trading strategies.

All you need is:

- A bank account

- KYC documents (PAN and Aadhaar)

- A few minutes on a mobile app like Zerodha, INDMoney, Groww or Kuvera.

And you can start investing in just a few clicks.

Mutual funds are beginner-friendly and can be accessed easily using mobile apps.

For example:

Think of mutual fund apps like WhatsApp or Instagram — simple, user-friendly, and accessible. Just like how you send messages or upload photos without any difficulty, you can also invest in mutual funds with just a few taps on your phone.

B. A Stepping Stone to Financial Growth

Mutual funds aren’t just for making quick money. They’re a tool to help you build wealth over time.

Whether you’re saving for a home, car, retirement, or your child’s education, mutual funds can help you reach those goals faster than traditional options like fixed deposits (FDs).

Plus, you can choose different types of funds based on your risk level and goals. More on that later!

Mutual funds act as a stepping stone to long-term financial planning and goal-based investing.

For example:

Imagine you’re saving for your child’s college education. If you put your money in a regular savings account, it might not grow fast enough to cover rising tuition fees. But if you invest in a mutual fund that matches your timeline, your money has the potential to grow significantly — helping you meet your goal comfortably.

C. Inspiring Real-Life Example: The Rs. 500/Month Story

Meet Ravi, a salaried employee in Mumbai. He started investing ₹500 every month in a mutual fund at age 25. By the time he turned 45, his investment had grown to over ₹3 lakh, even though he only invested ₹1.2 lakh total.

This shows how small, consistent investments can grow significantly over time.

Even modest monthly investments can grow into meaningful savings with time and discipline.

For example:

Ravi didn’t become rich overnight. He simply stayed consistent. Think of it like saving ₹500 every month to buy a new smartphone in 5 years. If you keep that money in a savings account, inflation will eat away its value. But if you invest it wisely, that ₹500/month could grow into something bigger — maybe even a laptop along with the phone!

4. Summary of This Section

This section explains why mutual funds make sense for beginners in India. Here’s what we’ve covered:

- Feeling nervous? You’re not alone. It’s perfectly normal to feel unsure when you first hear terms like “market” or “investment.” Mutual funds are made for people like you — no need to be an expert.

- Start small and start early. Time is your best friend. Even ₹500/month can grow into something significant over the years thanks to compounding.

- What is a mutual fund? It’s like a potluck dinner — many people contribute a little money, and together they get access to a variety of investments managed by a professional.

- Professionals handle the hard work. You don’t have to study stock charts or follow the news every day. A fund manager takes care of that for you.

- Mutual funds are simple and accessible. You can start with just a mobile app, a bank account, and basic documents like PAN and Aadhaar.

- They help you grow your money toward real-life goals. Whether it’s buying a home, funding your child’s education, or planning for retirement, mutual funds offer better growth than traditional options like FDs.

- Real-life success stories prove it works. People like Ravi show how consistency pays off — investing just ₹500/month can result in ₹3 lakh in 20 years.

In short, mutual funds are a great place to start your investment journey — even with small amounts. They help you grow your money safely, steadily, and with minimal effort on your part.

II. The Big Wins: Why Mutual Funds Stand Out for Indian Beginners

1. Professional Money Managers Work for You

A. Experts Handling Your Investments Daily

As a beginner, you might wonder: What if I pick the wrong stock or miss a market crash?

With mutual funds, you don’t have to worry about that. There’s a team of experienced fund managers who study markets, track trends, and make smart decisions on your behalf.

They spend hours researching companies, analyzing risks, and adjusting portfolios to give you the best possible returns.

You benefit from the expertise of trained professionals without having to do the hard work yourself.

For example:

Let’s say you want to invest in stocks but aren’t sure which ones to choose. A fund manager does all the research — they look at company performance, industry trends, and economic factors before deciding where to invest. You simply invest in the fund and let them handle the rest.

B. Less Stress for You as a New Investor

You can focus on your job, studies, or business while your money grows in the background. No need to panic during market dips — your fund manager is already managing the ups and downs.

Mutual funds reduce your stress by handling the complex parts of investing for you.

For example:

Imagine you invested in a stock, and suddenly there’s bad news about the company. The stock price drops, and you’re worried. With a mutual fund, the fund manager would decide whether to hold or sell based on long-term strategy — so you don’t have to make tough calls during market volatility.

2. Spreading Out Your Risk (Diversification)

A. Why Putting All Your Eggs in One Basket is Risky

Let’s say you invest all your money in just one company. If that company does well, great! But if it underperforms or crashes, you could lose a lot.

This is called concentration risk — and it’s dangerous for beginners.

Putting all your money in one place increases the risk of losing it all.

For example:

Suppose you invest ₹50,000 in a tech company. If that company performs poorly due to competition or poor management, your entire investment could be affected. But if your money was spread across multiple sectors like banking, healthcare, and energy, the impact of one sector falling wouldn’t hurt as much.

B. How Mutual Funds Invest in Many Places

Mutual funds spread your money across many companies and sectors. So, even if one company doesn’t do well, others may perform better, balancing out your overall returns.

For example, a fund might invest in IT, banking, pharmaceuticals, and consumer goods — giving you exposure to multiple industries with a single investment.

Diversification helps protect your money by spreading it across different areas.

For example:

Think of it like this: if you own a restaurant, and only serve biryani, you’re taking a big risk. What if people get tired of biryani or another restaurant offers better deals? But if you offer biryani, paneer tikka, and desserts, you’re not dependent on just one item.

Similarly, mutual funds diversify your investments so no single loss affects your entire portfolio.

3. Start Small, Grow Big (Affordability and SIPs)

A. Investing with as Little as ₹500 Through SIPs (Systematic Investment Plans)

One of the most powerful features of mutual funds is the SIP (Systematic Investment Plan).

With a SIP, you can invest a small fixed amount every month — say ₹500 or ₹1,000 — automatically from your bank account.

This makes investing simple, disciplined, and affordable.

SIPs allow you to start investing with as little as ₹500, making mutual funds accessible to everyone.

For example:

If you set up a monthly SIP of ₹500 in a mutual fund, over a year you’ll have invested ₹6,000. Over time, this small amount can grow significantly thanks to compounding.

You don’t need lakhs of rupees to begin — just a small, consistent effort.

B. The Power of Regular, Small Investments Over Time

Consistency beats timing. Even small, regular investments can beat big, one-time investments made later.

Let’s compare two people:

- Raj starts investing ₹1,000/month at age 25.

- Amit starts investing ₹2,000/month at age 35.

Both earn 12% returns.

By age 60:

- Raj has over ₹40 lakhs.

- Amit has around ₹30 lakhs.

Even though Raj invested less each month, he ended up with more because he started earlier.

Starting early and staying consistent beats waiting and investing larger amounts later.

For example:

Think of saving for a vacation. If you save ₹1,000 every month starting now, you’ll reach your goal faster than someone who waits two years and saves ₹2,000 per month. The same logic applies to investing — consistency matters more than the amount.

4. The Magic of Compounding: Your Money’s Best Friend

A. Earning Returns on Your Returns, Like a Snowball

Compounding is when your investment earns returns, and then those returns also start earning returns.

It’s like a snowball rolling down a hill — it starts small, but keeps growing as it moves forward.

The longer your money stays invested, the more it grows — not just linearly, but exponentially.

Compounding lets your money grow faster over time by earning returns on both your investment and the returns it generates.

For example:

Say you plant a tree and water it regularly. At first, nothing seems to happen. But after a few years, the tree grows tall and strong. Similarly, compounding works slowly at first, but once time passes, your money starts growing rapidly.

B. Real Indian Example: ₹1,000/Month Over Decades

Let’s take the earlier example again.

If you invest ₹1,000/month for 35 years at 12% annual returns, you’ll end up with over ₹40 lakhs.

That’s the power of Compounding + Consistency.

Small monthly investments can become big savings over decades due to compounding.

For example:

Meet Anil, a teacher in Delhi. He started investing ₹1,000/month in a mutual fund at age 25. By the time he turned 60, his investment had grown to ₹40+ lakhs. His secret? He didn’t stop investing — he stayed consistent and gave his money time to grow.

C. Case Study: Why Starting Early Makes a Huge Difference

Meet Priya and Neha:

- Priya starts investing ₹2,000/month at age 25.

- Neha starts investing ₹4,000/month at age 35.

Both invest until age 60.

At 12% returns:

- Priya ends up with ₹90+ lakhs.

- Neha ends up with ₹75+ lakhs.

Even though Neha invested twice as much each month, Priya still earned more — all because she started 10 years earlier.

Starting early gives you a head start that no amount of money can replace later.

For example:

Let’s say two friends plan to buy a car. One starts saving ₹2,000/month at age 25, and the other starts saving ₹4,000/month at age 35. By age 60, the one who started earlier will have saved more — not because they saved more money, but because they gave their money more time to grow.

5. Easy to Buy and Sell (Liquidity)

A. How You Can Get Your Money Back When Needed

Unlike real estate or fixed deposits, mutual funds are liquid, meaning you can withdraw your money whenever you need it (except for ELSS funds, which have a 3-year lock-in).

Most funds let you redeem your units online within minutes, and the money reaches your bank account in 1–3 working days.

Mutual funds offer easy access to your money compared to other investment options.

For example:

Imagine you need emergency funds for a medical situation. If your money is stuck in property or a fixed deposit, it might take weeks to get cash. But with mutual funds, you can log into your app, sell your units, and get your money in your bank within a couple of days.

B. Comparing with Other Indian Options Like Property or FDs

Fixed deposits (FDs) and property are popular in India, but they come with drawbacks:

- FDs offer low returns (around 5–7%) and early withdrawal penalties.

- Property is expensive and difficult to sell quickly.

Mutual funds strike a balance between growth and liquidity.

Mutual funds combine the benefits of growth and flexibility, unlike FDs or property.

For example:

If you put ₹1 lakh in an FD at 6% interest, you’ll earn ₹6,000 per year. But if you invest that same ₹1 lakh in a mutual fund earning 12% annually, you’ll double your money in about 6 years. Plus, you can withdraw it anytime — something FDs and property can’t easily offer.

6. Clear and Simple Rules (Transparency & Regulation by SEBI)

A. Why SEBI (Securities and Exchange Board of India) Protects You

Mutual funds in India are regulated by SEBI, which ensures that:

- Fund houses follow strict rules.

- Investors’ interests are protected.

- Information is transparent and fair.

This means you can trust that your money is being managed responsibly.

SEBI regulations ensure mutual funds are safe, transparent, and investor-friendly.

For example:

Just like how traffic police ensure road safety, SEBI ensures financial safety in the world of investing. They monitor fund companies, check their practices, and prevent fraud — so you know your money is in good hands.

B. Easy Access to Fund Information and Performance

Every mutual fund must publish its performance, portfolio, and fees regularly. You can check these details anytime on platforms like Zerodha, INDMoney, Groww and Kuvera.

You’ll always know where your money is invested and how it’s performing.

Mutual funds provide full transparency, so you always know how your investment is doing.

For example:

Before buying a phone, you probably check its specs and reviews. Similarly, with mutual funds, you can see exactly what the fund invests in, how much it charges, and how well it has performed over time — all available with a few clicks on your phone.

C. Trust-Building: The “Mutual Funds Sahi Hai” Campaign by AMFI

The AMFI (Association of Mutual Funds in India) launched the famous campaign “Mutual Funds Sahi Hai” to educate people about the safety and benefits of mutual funds.

Through TV ads, social media, and local campaigns, they’ve helped millions of Indians feel confident about investing.

Initiatives like “Mutual Funds Sahi Hai” are helping build trust and awareness among Indian investors.

For example:

If you’ve seen ads showing families investing together or young professionals planning for their future through mutual funds, that’s part of the “Mutual Funds Sahi Hai” movement. It’s designed to make investing feel normal, safe, and beneficial for everyone — especially beginners.

7. Tax Benefits (Where Applicable)

A. Understanding ELSS (Equity-Linked Savings Schemes) for Tax Saving

Some mutual funds, called ELSS, offer tax benefits under Section 80C of the Income Tax Act.

You can save up to ₹1.5 lakh per year in taxes by investing in ELSS funds.

However, there’s a 3-year lock-in period, which means you can’t withdraw your money during that time.

ELSS funds let you save tax while growing your money through equity investments.

For example:

If you earn ₹10 lakh per year and invest ₹1.5 lakh in an ELSS fund, your taxable income reduces to ₹8.5 lakh. That means you pay less tax and grow your money at the same time — a win-win!

B. Other Tax Considerations for Indian Investors

Different types of mutual funds have different tax rules:

- Equity funds: Long-term gains up to ₹1 lakh are tax-free; above that, taxed at 12.5%.

- Debt funds: Gains are taxed based on your income tax slab or at 20% with indexation after 3 years.

Understanding these rules helps you plan your investments wisely.

Knowing tax rules helps you maximize your post-tax returns from mutual funds.

For example:

Let’s say you invested ₹1 lakh in an equity fund and sold it later for ₹1.5 lakh. Since your gain is ₹50,000 and below the ₹1 lakh tax-free limit, you don’t have to pay any tax. But if your gain was ₹1.2 lakh, you’d pay 12.5% tax only on the amount above ₹1 lakh — which is ₹20,000 in this case.

8. Summary of This Section

- Professional money managers work for you – experts handle your investments so you don’t have to stress about market fluctuations.

- Diversification spreads your risk – instead of putting all your money in one place, mutual funds spread it across multiple companies and sectors.

- Start small with SIPs – invest as little as ₹500/month and grow your wealth consistently.

- Compounding grows your money faster – the longer you stay invested, the more your money multiplies.

- Mutual funds are liquid – unlike property or FDs, you can easily get your money back when needed.

- Regulated by SEBI for safety – mutual funds follow strict rules and offer full transparency.

- Tax benefits with ELSS funds – save tax while growing your money through equity-linked schemes.

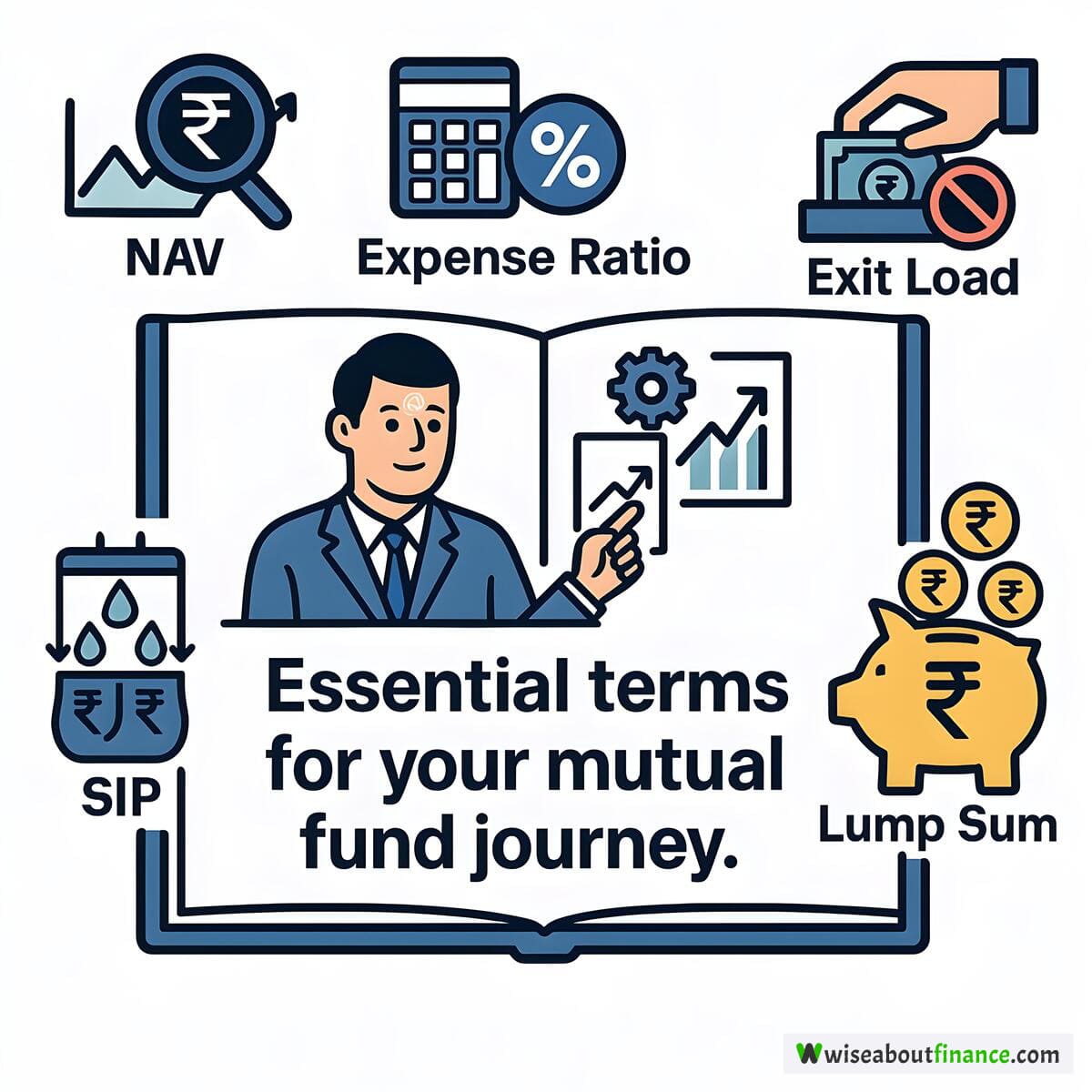

III. Getting Started: Key Terms Every Indian Beginner Should Know

When you start investing in mutual funds, it’s important to understand some basic terms. These words might sound confusing at first, but once you know what they mean, everything becomes much clearer. Let’s break them down one by one with simple examples from everyday life.

NAV stands for Net Asset Value. Think of it like the price tag on a product — but instead of a shirt or a phone, this price tag is for a unit of a mutual fund.

Each day, the value of a mutual fund changes depending on how well the stocks or bonds inside the fund are doing.

NAV tells you the current value of each unit in a mutual fund.

For example:

Let’s say you want to buy a packet of biscuits. The packet costs ₹20. That’s like the NAV of that packet. If tomorrow the same packet costs ₹22, its “NAV” has gone up. Similarly, if a mutual fund’s NAV was ₹10 today and becomes ₹11 tomorrow, your investment has grown by ₹1 per unit.

Since mutual funds invest in assets like stocks and bonds, which go up and down every day, the NAV also changes daily.

You can check the latest NAV on platforms like Groww or Kuvera.

Your investment grows or falls based on the changing NAV of the fund.

For example:

Think of NAV like petrol prices. One day petrol is ₹100 per litre, the next day it’s ₹102. Similarly, a mutual fund’s NAV could be ₹20 today and ₹20.50 tomorrow. This change shows whether your investment is growing or shrinking.

2. Expense Ratio: What You Pay the Fund Manager

A. Understanding the Small Annual Fee

The expense ratio is the small fee you pay every year to the fund house for managing your money. It covers things like:

- Research

- Salaries of experts

- Marketing

It’s usually around 0.5% to 1.5% of your investment.

The expense ratio is a small fee you pay for the fund manager’s services.

For example:

Let’s say you invest ₹10,000 in a fund with an expense ratio of 1%. That means ₹100 of your money goes toward paying for the fund’s management, and ₹9,900 is invested in stocks or bonds.

B. Why a Lower Expense Ratio is Generally Better

Even a small fee adds up over time. So, funds with lower expense ratios give you more returns in the long run.

A lower expense ratio means more of your money stays invested and grows.

For example:

Imagine two ice cream vendors:

- Vendor A charges ₹1 extra per cone.

- Vendor B gives the same cone without any extra charge.

Who would you choose? Probably Vendor B. Same logic applies to mutual funds — pick funds with lower fees so you keep more of your profits.

3. Exit Load: A Small Fee if You Leave Early

A. When This Charge Applies

Sometimes, if you withdraw your money too soon (usually within 6–12 months), the fund charges a small fee called an exit load.

This is done to discourage people from pulling out their money too early.

An exit load is a small fee you pay if you withdraw your money too early.

For example:

Let’s say you invest ₹10,000 and decide to take your money out after 3 months. Some funds may charge 0.5% as an exit load, which means you’ll get back only ₹9,950.

B. How to Avoid It

Just hold your investment for the minimum time required — often 6 to 12 months — and the exit load won’t apply.

Avoid exit loads by keeping your money invested for at least the minimum holding period.

For example:

If you’re buying a mobile phone on EMI, you agree to pay for 12 months. If you stop paying early, there might be a penalty. Similarly, wait until the fund says it’s okay to withdraw — and avoid paying extra fees.

4. Fund Manager: Your Investment Expert

A. Their Role in Picking Stocks and Bonds

A fund manager is like a chef who decides what ingredients to use in a dish. They decide where to invest your pooled money — in stocks, bonds, or other assets — to get the best possible returns.

They research companies, track market trends, and make smart decisions.

Fund managers make smart investment decisions on your behalf.

For example:

If you’re planning a birthday party, you might ask your friend to help you choose the venue and food. In mutual funds, the fund manager does the same — picks the best investments so you don’t have to worry about it.

B. Why Their Experience Matters

An experienced fund manager knows how to handle ups and downs in the market. They’ve seen tough times before and know when to stay calm and when to act.

A skilled fund manager can make a big difference in your investment’s performance.

For example:

Let’s say you’re learning to drive. Would you prefer a new driver or someone who’s been driving for years? Probably the experienced one. Similarly, a seasoned fund manager helps protect and grow your money better than someone just starting out.

5. SIP: Your Best Friend for Regular Investing

A. Automating Your Investments Each Month

SIP (Systematic Investment Plan) lets you invest a fixed amount every month automatically. It’s like setting up a monthly reminder to save money for something special.

This builds discipline and removes guesswork.

SIP helps you invest regularly without effort.

For example:

If you set up a SIP of ₹500/month, you’ll invest that amount every month without having to remember it — just like your Netflix subscription auto-debits every month.

B. The Benefit of “Rupee Cost Averaging”

With SIP, you buy more units when prices are low and fewer when prices are high. Over time, this averages out your cost.

SIP helps you buy mutual fund units at an average price, reducing the impact of market fluctuations.

For example:

Think of it like buying onions every week. Sometimes onions cost ₹20/kg, sometimes ₹30/kg. If you buy them weekly, your average cost will be somewhere in the middle. SIP works the same way — smoothing out the highs and lows of the market.

6. Lump Sum: Investing All at Once

A. When a One-Time Investment Makes Sense

If you suddenly get a large amount of money — like a bonus, gift, or savings from selling gold — you might consider investing it all at once. That’s called a lump sum investment.

It works best when you feel the market is undervalued.

A lump sum investment is useful when you have a large amount to invest immediately.

For example:

Let’s say you got a Diwali bonus of ₹50,000. Instead of waiting to invest it slowly, you could put the whole amount into a mutual fund right away if you believe it’s a good time to do so.

B. Combining SIPs and Lump Sum

Many investors use both approaches — invest a lump sum now and continue with SIPs for regular contributions.

This gives you immediate growth and steady discipline.

Combining lump sum and SIP investments helps you grow money faster and consistently.

For example:

Say you got ₹50,000 from your savings and decide to invest it all now. Then, you also set up a monthly SIP of ₹1,000. Now, your money starts working for you right away, and keeps growing every month.

7. Summary of This Section

In this section, we covered the key terms every beginner should know before investing in mutual funds:

- NAV tells you how much each unit of your fund is worth. It changes every day like petrol prices.

- Expense ratio is a small annual fee you pay to the fund manager. Lower fees mean more money stays invested and grows.

- Exit load is a small charge if you withdraw your money too early. Wait for the minimum holding period to avoid it.

- Fund managers are the professionals who pick the best investments for you. Their experience matters a lot.

- SIP (Systematic Investment Plan) lets you invest small amounts every month, making investing disciplined and stress-free.

- Lump sum is when you invest a large amount all at once — great for bonuses or sudden windfalls.

- You can combine SIP and lump sum to grow your money quickly and steadily.

Whether you’re investing through SIPs, lump sums, or a mix of both, knowing how NAV, expense ratio, exit load, and fund managers work helps you make better choices.

So, take your time, learn step by step, and soon you’ll feel confident about managing your own investments.

IV. Finding Your Fit: Types of Mutual Funds for Indian Beginners

1. Equity Funds: Investing in Companies for Growth

A. Large Cap, Mid Cap, Small Cap – What’s the Difference for Growth Potential

Equity funds invest in stocks of companies. Based on the size of the company, they are categorized as:

- Large Cap: Top 100 companies (most stable)

- Mid Cap: Companies ranked 101–250 (moderate risk, moderate growth)

- Small Cap: Companies ranked beyond 250 (higher risk, higher potential growth)

Choose based on your risk appetite — large caps are safer, small caps are riskier but potentially more rewarding.

For example:

Think of it like this — investing in a big brand like Reliance or Tata is like buying gold jewelry from a trusted jeweler — it’s safe and reliable. But investing in a small startup is like trying a new restaurant — there’s more risk, but if it becomes popular, you could get great value later.

B. Funds that Invest in Indian Stocks

There are several equity funds focused entirely on Indian companies, such as:

- HDFC Equity Fund

- ICICI Prudential Bluechip Fund

- Axis Bluechip Fund

These are great for long-term wealth creation.

Indian-focused equity funds let you grow your money by investing in our country’s top businesses.

For example:

If you believe in India’s growth story and want to benefit from its rising companies, these funds are perfect. Just like how Flipkart grew over the years, many Indian companies have given great returns to investors who stayed invested for the long term.

2. Debt Funds: Safer Bets for Steady Returns

A. Investing in Government Bonds and Company Loans

Debt funds invest in government bonds, corporate deposits, and other fixed-income instruments. They are less risky than equity funds.

Debt funds are safer and give predictable returns, like FDs but often better.

For example:

Imagine lending ₹1 lakh to a friend who promises to pay back with interest every year. That’s what debt funds do — they lend money to governments or companies and earn regular interest.

B. Comparing with Fixed Deposits (FDs) and PPF (Public Provident Fund)

| Option | Risk | Returns | Liquidity |

|---|---|---|---|

| FD | Low | 5–7% | Medium |

| PPF | Low | 7–8% | Low |

| Debt Fund | Low-Moderate | 7–9% | High |

Debt funds often give better returns than FDs and PPF, with more liquidity.

For example:

Let’s say you have ₹5 lakh and want to invest safely. If you put it in an FD giving 6%, you’ll earn ₹30,000 per year. But if you invest in a debt fund giving 8%, you’ll earn ₹40,000 — more return with almost similar safety. Plus, you can withdraw anytime, unlike PPF which locks your money for 15 years.

3. Hybrid Funds: A Mix of Both Worlds

A. Balancing Risk and Return with Stocks and Bonds

Hybrid funds mix equity and debt, offering a middle path. They are good for those who want some growth but don’t want to take full risk.

Hybrid funds give you a balanced approach — part growth, part safety.

For example:

It’s like eating both dal and sabzi at a meal — one gives protein, the other gives fiber. Similarly, hybrid funds give you a mix of stock growth and bond stability.

B. Suitable for Moderate Risk-Takers

Examples include:

- Balanced Advantage Funds

- Aggressive Hybrid Funds

- Conservative Hybrid Funds

Choose based on how much risk you can handle.

Hybrid funds suit investors who want a mix of safety and growth.

For example:

If you’re not sure whether to go all-in on equity or stick to debt, hybrid funds offer the best of both worlds. Conservative hybrid funds keep most of your money in safe bonds, while aggressive ones lean toward stocks. Balanced advantage funds adjust automatically based on market conditions.

4. Index Funds: Simple and Low Cost

A. Tracking Market Indices like Nifty 50 or Sensex

Index funds replicate popular indices like Nifty 50 or Sensex. They don’t try to beat the market — they simply follow it.

Index funds give you market returns at a very low cost.

For example:

Imagine you own a small piece of every company in the Nifty 50. Whether it’s Infosys, HDFC Bank, or TCS, you grow along with them without worrying about picking winners or losers.

B. Passive Investing for Long-Term Growth

Since they don’t require active management, their expense ratio is very low — often below 0.2%.

Index funds are perfect for long-term investors who want simplicity and low fees.

For example:

Let’s say you invest ₹10,000 in an index fund tracking Nifty 50. If Nifty grows by 12% in a year, your investment will also grow by around 12%. No need to track individual stocks — just follow the market and save on fees.

5. ELSS Funds: Saving Taxes and Investing

A. The Dual Benefit of Tax Savings Under Section 80C

ELSS funds let you save up to ₹1.5 lakh in taxes under Section 80C.

ELSS funds offer tax benefits along with long-term growth.

For example:

If you earn ₹10 lakh per year and invest ₹1.5 lakh in ELSS, your taxable income drops to ₹8.5 lakh. You save tax and grow your money at the same time.

B. The 3-Year Lock-in Period

You cannot withdraw your money for 3 years, but this also ensures long-term investing.

ELSS funds are ideal for tax-saving and wealth-building together.

For example:

Just like a fixed deposit has a lock-in period, ELSS funds ask you to stay invested for 3 years. This helps you avoid impulsive decisions and grow your money steadily.

6. Summary of This Section

- Equity funds invest in company stocks. You can choose between large cap (safe), mid cap (balanced), and small cap (high risk, high reward).

- Debt funds are safer and give steady returns by investing in bonds and loans. They often beat FDs and PPF in returns and liquidity.

- Hybrid funds combine equity and debt, offering a balanced mix for moderate-risk investors.

- Index funds follow major market indices like Nifty 50 or Sensex. They’re simple, low-cost, and great for long-term growth.

- ELSS funds help you save tax under Section 80C and grow your money through equity investments. They come with a 3-year lock-in, encouraging discipline.

By understanding these options, you can pick the right mutual fund that fits your financial goals and comfort with risk.

Whether you’re saving for a home, retirement, or just growing your money, mutual funds give you flexible choices that work for you.

V. Your First Steps: How to Invest in Mutual Funds in India

You’ve decided to start investing — great choice!

Now, let’s walk through the 7 simple steps that will help you begin your mutual fund journey in India.

We’ll take it one step at a time, with real-life examples and easy-to-understand language so everything feels clear and doable.

1. Step 1: Figure Out Your Goals (Why Are You Investing?)

A. Short-Term vs. Long-Term Goals (e.g., Car, Home, Retirement)

Before you start investing, ask yourself: What are you saving for?

Your goal could be:

- Buying a car or home

- Going on a dream vacation

- Paying for higher education

- Saving for retirement

Short-term goals usually last 1–3 years, while long-term goals go beyond 5–10 years.

Knowing your goal helps you choose the right mutual fund and how long to invest.

For example:

Let’s say you want to buy a bike worth ₹1 lakh in 2 years. That’s a short-term goal, so you might choose a debt fund. But if you’re saving for your child’s college education in 15 years, that’s a long-term goal — and equity funds may be better suited for growth.

B. Setting Clear Financial Targets

Let’s say you want to save ₹10 lakh for a down payment on a house in 5 years.

You can calculate how much to invest each month to reach that target using tools like SIP calculators.

Set clear targets so you know exactly what you’re working toward.

For example:

Use an online SIP calculator to find out how much you need to invest monthly to reach ₹10 lakh in 5 years. If the expected return is 12%, you’d need to invest around ₹11,000 per month. This gives you a clear plan to follow.

2. Step 2: Know Your Risk Comfort Zone

A. Understanding Your Willingness to Take Risks

Some people are okay with their investment going up and down — others prefer more stability.

Think about this:

- If your investment drops by 10% in a month, would you panic and sell?

- Or would you stay calm and wait for it to grow again?

This helps you understand your risk tolerance.

Don’t invest in something that makes you nervous — match your risk level with the right fund.

For example:

Imagine you invested ₹50,000 and after a few months, it goes down to ₹45,000. Would you feel stressed and pull your money out? If yes, you might be a low-risk investor. If not, you might be comfortable with higher risk and higher potential returns.

B. Matching Funds to Your Risk Profile

Here’s a quick guide:

| Risk Level | Suitable Fund Types |

|---|---|

| Low | Debt funds, PPF |

| Medium | Hybrid funds |

| High | Equity funds |

Choose a fund type that matches your comfort with market ups and downs.

For example:

If you’re someone who likes steady growth without big surprises, debt funds might be perfect for you. But if you’re okay with some ups and downs and want faster growth, equity funds could be the way to go.

3. Step 3: Pick the Right Fund for You

A. Simple Tips for Fund Selection

When choosing a mutual fund, look at:

- Past performance (not just returns, but consistency)

- Expense ratio (lower is better)

- Fund manager experience

- Asset size (not too small, not too big)

Use platforms like Groww or Zerodha to compare funds easily.

Look at more than just returns — pick a fund that fits your goals and risk profile.

For example:

If two funds gave similar returns last year, but one has a lower expense ratio and a more experienced fund manager, that’s probably the better choice for long-term growth.

B. Looking at Fund Performance and Consistency

Don’t just chase high returns from one year.

Check if the fund has performed well over 3–5 years.

For example, if a fund gave 20% return last year but only 5% the previous year, it might be inconsistent.

Choose funds that give steady, consistent growth over time.

For example:

Think of it like hiring an employee. Would you choose someone who did extremely well once but underperformed the rest of the time — or someone who delivered good results consistently? The same logic applies to mutual funds.

4. Step 4: Complete Your KYC (Know Your Customer) – It’s Mandatory!

A. Documents Needed (PAN, Aadhaar, Bank Statement)

To invest in mutual funds, you must complete KYC (Know Your Customer) verification.

You’ll need:

- PAN card

- Aadhaar card

- Bank statement

- Income proof (if applicable)

- Passport-sized photo

KYC is a one-time process and required by law.

For example:

It’s just like verifying your identity when opening a bank account. Once done, you can invest in any mutual fund across all platforms.

B. The Role of KRA (KYC Registration Agency)

KYC is handled by KRA (KYC Registration Agencies) like CVL KRA or CDSL Ventures.

Most online platforms help you do this digitally — no need to visit an office.

Once your KYC is done, you can invest across all mutual funds without repeating the process.

For example:

Just like how you upload your documents once to open a savings account, KYC needs to be done only once before starting your mutual fund investments.

5. Step 5: Choose Your Investment Platform (Online vs. Offline)

A. Popular Indian Online Platforms: Zerodha, Groww, INDMoney, Kuvera

These apps make investing easy:

- Compare funds

- Start SIPs in minutes

- Track your investments anytime

- Get alerts and updates

Online platforms offer convenience, transparency, and low fees.

For example:

Think of these platforms like Flipkart or Swiggy — user-friendly, fast, and packed with helpful features. Just like ordering food or shopping online, you can now invest in mutual funds with just a few taps on your phone.

B. Why “Direct” Funds Can Be Better Than “Regular” Funds

There are two types of mutual funds:

- Direct Plans: No commission paid to agents → lower expense ratio → higher returns

- Regular Plans: Commission included → slightly higher expense ratio → slightly lower returns

Always choose direct plans unless you’re taking expert advice.

Direct plans help you earn more returns over time.

For example:

Imagine buying a shirt directly from the factory versus through a middleman. In the first case, you pay less because there’s no extra commission. Similarly, direct mutual funds have lower fees, which means more money stays invested and grows for you.

C. Investing Through a Financial Advisor

If you’re unsure where to start, a certified financial advisor can guide you. But remember:

- They may recommend regular plans (to earn commission)

- Make sure they’re SEBI-registered or AMFI-certified

Advisors can help, but always understand what you’re investing in.

For example:

It’s like visiting a doctor — you should listen to their advice, but also ask questions and understand what’s best for your health. Same with advisors — take guidance, but don’t blindly follow recommendations.

6. Step 6: Start Your SIP (or Lump Sum)

A. Setting Up Your First Automated Investment

Starting a SIP is simple:

- Log in to your chosen platform (Zerodha, INDMoney, Groww, Kuvera).

- Search for the fund you want.

- Click “Invest”.

- Select “SIP”.

- Choose amount and date.

- Confirm and link your bank account.

That’s it! Your money will be invested automatically every month.

SIPs help you build discipline and grow wealth steadily.

For example:

Setting up a SIP is just like setting a recurring payment for your mobile recharge. Once set, it happens automatically — helping you stay consistent and grow your money over time.

B. How to Make a One-Time Investment

If you have a lump sum (like a bonus or savings), you can invest it all at once:

- Open your app.

- Search for the fund.

- Click “Invest”.

- Choose “One-time”.

- Enter amount.

- Confirm.

Make sure the fund aligns with your goal and risk level.

Lump sum works best when you have a large amount and believe markets are undervalued.

For example:

Let’s say you received ₹2 lakh as a bonus and believe it’s a good time to invest. You can use a one-time investment to put that money into a mutual fund and watch it grow.

7. Step 7: Keep an Eye on Your Investment

A. How to Monitor Your Fund’s Performance

Don’t just set and forget.

Check your portfolio every 3–6 months to see:

- Is the fund still performing well?

- Has the fund manager changed?

- Does it still fit your goals?

You can use the same app to track your investments.

Regular check-ins ensure your investments stay on track.

For example:

Just like checking your WhatsApp messages regularly, you should review your mutual fund investments every few months to make sure everything is growing as planned.

B. Understanding Your Investment Statement

Every investor gets a Consolidated Account Statement (CAS) monthly or quarterly.

The CAS shows:

- All your mutual fund holdings

- Returns earned

- Transaction history

Use platforms like MF Central to view all your investments in one place.

Stay informed and make decisions based on facts, not emotions.

For example:

Your CAS is like a report card for your investments. It tells you how each fund is doing and whether you’re moving closer to your financial goals.

8. Summary of This Section

In this section, we walked through the practical steps to start investing in mutual funds in India. Here’s a quick recap:

- Figure out your goals – Whether it’s for a new car, your child’s education, or retirement, knowing your goal helps you pick the right fund.

- Understand your risk profile – Match your comfort with market fluctuations to choose the right kind of fund — low, medium, or high risk.

- Pick the right fund – Look at past performance, expense ratio, fund manager experience, and asset size before choosing.

- Complete your KYC – This is mandatory and one-time. Use platforms like Groww or Zerodha to do it digitally.

- Choose your investment platform wisely – Opt for trusted apps like Groww, Zerodha, INDMoney, or Kuvera. Always choose direct plans to save on fees.

- Start your SIP or make a lump sum investment – SIPs help you invest regularly; lump sums work well when you have a large amount ready to go.

- Monitor your investments – Review your portfolio every 3–6 months and keep an eye on your Consolidated Account Statement (CAS) to track progress.

Whether you’re investing ₹500/month or ₹1 lakh in one go, the key is to start — and stay consistent. Over time, your money will grow, thanks to smart choices and regular check-ins.

Now that you’ve completed this section, you’re well on your way to becoming a confident mutual fund investor.

Let’s move on to the next part, where we’ll discuss important checks and common mistakes to avoid.

VI. Investing Smart: Important Checks & Avoiding Common Mistakes

Now that you understand the basics of mutual funds and how fund managers work, it’s time to learn how to invest smart and avoid common mistakes many beginners make in India.

This section will help you:

- Know what documents to check before investing

- Understand how risky a fund is

- Stay invested for long-term growth

- Avoid costly errors like panic selling or chasing returns

Let’s go step by step.

1. Important Checks for Proactive Investing

A. Reading the Offer Document (SID and KIM)

Every mutual fund comes with two important documents:

- SID (Scheme Information Document) – Explains what the fund invests in, its goals, and risks.

- KIM (Key Information Memorandum) – Gives a quick summary of fees, returns, and performance.

These are like the user manual of your investment — they tell you everything you need to know before putting your money in.

Understand your fund before putting your money in.

For example:

Think of it like reading reviews before buying a phone or checking the ingredients before eating something new. If you don’t read these documents, you might end up investing in something that doesn’t suit your needs.

B. Understanding Your Fund’s Risk Meter (The “Risk-o-meter”)

Each mutual fund has a risk meter from 1 to 5:

- 1 = Very low risk

- 2–3 = Medium risk

- 4–5 = High risk

This helps you see how risky the fund is before you invest.

Use the risk-o-meter to avoid investing in funds that are too risky for you.

For example:

If you’re someone who gets worried when your investment goes down even a little, look for funds with a 1 or 2 on the risk-o-meter. But if you can handle some ups and downs, a 3 or 4 might be okay.

C. The Importance of Long-Term Investing for Real Growth

Markets go up and down all the time.

If you pull out during a dip, you could lock in losses. But if you stay invested, the market usually recovers and grows over time.

This is called compounding — where your money earns more money over the years.

Time in the market beats timing the market.

For example:

Imagine you bought ice cream at ₹20 per scoop. Next week, it went up to ₹25 — great! But then it dropped to ₹18 for a few days. If you sold during that drop, you’d lose money. But if you waited, the price would likely rise again.

Same with mutual funds — staying invested pays off.

2. Common Mistakes Indian Beginners Must Avoid

A. Waiting Too Long to Start Investing

Many people think they need a large sum or perfect timing to begin.

But the truth is: even ₹500/month is enough to start, and the earlier you begin, the better.

Compounding works best when you give it time.

The best time to start investing is now.

For example:

Let’s say two friends — Anil and Sunil — both earn the same salary. Anil starts investing ₹500/month at age 25, while Sunil waits until he’s 35. By age 60, Anil ends up with twice as much money — just because he started early.

B. Stopping SIPs During Market Ups and Downs (Panic Selling)

Market fluctuations are normal — sometimes prices go up, sometimes they go down.

Stopping your SIP during a downturn means you miss the chance to buy units at lower prices.

Stick to your plan and keep investing regularly.

Stay calm and keep investing regularly.

For example:

It’s like going to the market every week to buy vegetables. Sometimes tomatoes cost ₹20/kg, sometimes ₹30/kg. If you stop buying just because tomatoes got expensive one week, you’ll miss cheaper prices later.

SIPs work the same way — keep investing, no matter what.

C. Investing Without a Clear Goal or Plan

Putting money into mutual funds without knowing why leads to confusion later.

Ask yourself:

- Why am I investing?

- When will I need this money?

Having a clear goal makes it easier to choose the right fund and stick with it.

Have a plan — know what you’re saving for and when you’ll need the money.

For example:

Suppose you want to save for your child’s education in 15 years. You wouldn’t pick a high-risk fund meant for short-term gains. Instead, you’d choose a balanced or equity fund that gives steady growth over time.

D. Not Doing Your Homework (Research Beyond Tips)

Don’t rely only on tips from social media or WhatsApp forwards.

Do your own research about:

- What the fund invests in

- Its past performance

- Who manages it

You can use platforms like Groww or Zerodha to compare funds easily.

Educate yourself before making any investment decision.

For example:

If a friend tells you to invest in a fund “because it gave 20% returns last year,” don’t jump in blindly. Check what it invests in, whether it matches your risk level, and how it performed over 3–5 years — not just one good year.

E. Chasing Only Past Returns (Focus on Consistency Instead)

A fund that gave great returns last year may underperform next year.

Look for consistent performance over time, not just one-time highs.

Choose funds that perform well across market conditions.

Focus on stable, long-term performance rather than short bursts of high returns.

For example:

Imagine you’re hiring an employee. Would you prefer someone who did extremely well once but underperformed the rest of the time, or someone who consistently delivered good results? Same logic applies to mutual funds.

F. Falling for “Get Rich Quick” Schemes

Be careful of schemes that promise unusually high returns in a short time.

Real investing grows your money slowly and safely — not overnight.

Stick to trusted mutual funds and avoid risky shortcuts.

If it sounds too good to be true, it probably is.

For example:

Someone might tell you about a scheme that says you’ll double your money in 6 months. That sounds tempting, but real investing isn’t like gambling — it’s about discipline, patience, and planning for the future.

G. Ignoring Your Nominee Details and Other Formalities

Make sure your nominee details (like spouse, parent, or child) are updated.

Also, ensure your mobile number and email are current with your investment platform.

This protects your investment and ensures smooth transfer in case of emergencies.

Small formalities protect your investment for the future.

For example:

If you pass away suddenly, your family won’t get your mutual fund money unless your nominee details are correct. Just like updating your bank nominee, it’s equally important here.

3. Summary of This Section

In this section, we learned how to invest smartly and avoid costly mistakes:

- Always read the SID and KIM before investing — they explain the fund’s goals, risks, and costs.

- Use the risk-o-meter to match your comfort level with the fund’s risk.

- Don’t panic during market dips — long-term investing lets compounding work its magic.

- Don’t wait to start — even small amounts grow significantly over time.

- Never stop your SIPs during market lows — you miss out on cheaper units.

- Set clear financial goals — this helps you choose the right fund and track progress.

- Do your homework — don’t follow tips blindly; research and verify.

- Avoid chasing short-term high returns — focus on consistent performance.

- Be cautious of “get rich quick” schemes — real investing takes time and discipline.

- Update your nominee details and personal information regularly — it protects your investments.

By following these checks and avoiding common mistakes, you’ll become a smarter, more confident investor — even as a beginner.

VII. Real-Life Investment Journeys for Indian Beginners

So far, we’ve learned how mutual fund managers work and why mutual funds are great for beginners in India. Now let’s look at real-life examples of people like you who have started investing — and see how mutual funds helped them reach their goals.

These stories will help you understand:

- How different types of people use mutual funds

- How small investments grow over time

- How to plan your own investment journey

Let’s go through each one step by step.

1. College Students Starting with Small SIPs

A. Building Discipline and Early Wealth

Meet Ananya, a final-year student who started investing ₹500/month through SIPs. By the time she got her first job, she already had ₹1.5 lakh saved — all from small, regular investments.

Even as a student, you can begin building wealth and financial habits early.

For example:

Let’s say you get a part-time job or receive pocket money regularly. You can set up a monthly SIP of ₹200–₹500 and watch it grow while you study. This teaches discipline and gives you a head start on financial freedom.

B. Saving for Higher Education or First Big Purchase

Ananya is now saving for her postgraduate studies abroad. Her SIPs are helping her build a strong financial foundation.

Start early — even small amounts grow significantly over time.

For example:

If you want to buy your dream laptop after graduation, start investing now. If you invest ₹300/month for 4 years at 12% returns, you’ll have around ₹18,000 ready when you need it — without having to borrow money.

2. Young Salaried Professionals Planning for Big Milestones

A. Saving for Marriage, Down Payment for a Home, or a New Car

Rohan, a software engineer in Bangalore, started investing ₹2,000/month after his first salary. He’s aiming to buy a house in 8 years. His SIPs are growing steadily, and he’s confident he’ll meet his goal.

Use mutual funds to plan for major life milestones.

For example:

You just landed your first job and earn ₹30,000/month. If you start investing ₹2,000 every month right away, by the time you’re 35, you could have over ₹5 lakhs — enough for a down payment or wedding expenses.

B. Using Mutual Funds for Medium to Long-Term Goals

Rohan chose hybrid funds to balance growth and safety. He reviews his portfolio annually and adjusts as needed.

Tailor your investments to your timeline and goals.

For example:

If you’re planning to buy a car in 3 years, you might choose a debt fund that’s safer. But if you’re saving for retirement 30 years away, equity funds may be better for faster growth.

3. Small Business Owners Looking to Beat Inflation

A. Growing Business Savings Systematically

Priya runs a boutique in Jaipur. She uses mutual funds to grow her business savings instead of keeping money idle in a savings account.

Beat inflation and grow your money smarter than traditional savings.

For example:

Imagine you run a small shop and save ₹10,000 every month. If you keep it in a savings account (4–5% interest), it grows slowly. But if you invest in a debt fund (7–9%), you make more money without taking too much risk.

B. Creating a Financial Safety Net

She also invests in debt funds for emergencies. This way, she has a backup without losing value to inflation.

Protect your business with smart investment choices.

For example:

Just like you keep emergency cash at home, Priya keeps some of her money in debt funds — easily accessible but earning more than a regular bank account.

4. Homemakers Investing from Household Savings

A. Empowering Financial Independence

Meena, a homemaker in Pune, started investing part of her household budget into mutual funds. Over 10 years, she built a corpus of ₹10 lakhs, which she now uses for family expenses and travel.

Financial independence starts with small, consistent steps.

For example:

Let’s say you manage the household and have some extra money left each month. You can start investing ₹1,000–₹2,000/month in mutual funds. Over time, that adds up — giving you control over your finances.

B. Building a Corpus for Family Goals

She used SIPs to plan for her children’s education and her own emergency fund.

Investing helps secure your family’s future and your own.

For example:

Instead of keeping extra money in fixed deposits, Meena chose mutual funds that gave better returns. That helped her create a bigger fund for her kids’ higher education — without stress.

5. Retired Individuals Using SWP for Monthly Income

A. Systematic Withdrawal Plan for Regular Payouts

Mr. Sharma, a retired teacher, invested in mutual funds during his working years. Now, he uses SWP (Systematic Withdrawal Plan) to get a fixed monthly income.

SWPs provide predictable income without touching your principal.

For example:

Think of SWP like a pension. Every month, Mr. Sharma gets ₹10,000 automatically credited to his account — even though he’s not working anymore.

B. Managing Post-Retirement Expenses

He keeps most of his money in debt and hybrid funds to ensure steady returns.

Mutual funds can support you throughout your life — even after retirement.

For example:

When you retire, your salary stops — but your expenses don’t. By staying invested in safe funds, Mr. Sharma ensures he always has money coming in to cover medical bills, travel, or daily needs.

6. Summary of This Section

In this section, we looked at real-life journeys of Indian beginners who started investing in mutual funds:

- Students like Ananya started early with small SIPs and grew meaningful savings before their careers even began.

- Young professionals like Rohan used mutual funds to plan for big goals such as buying a house or getting married.

- Small business owners like Priya made smart decisions to beat inflation and protect their hard-earned money.

- Homemakers like Meena turned monthly savings into a large financial cushion — giving them confidence and control.

- Retirees like Mr. Sharma continue to benefit from mutual funds through monthly withdrawals, ensuring financial security in their later years.

No matter who you are — whether you’re studying, working, running a business, managing a home, or enjoying retirement — mutual funds offer something for everyone. They help you grow your money safely, stay ahead of inflation, and achieve personal goals with ease.

All it takes is consistency, a little knowledge, and the willingness to start small. And once you do, your money works for you — no matter what stage of life you’re in.

VIII. Helpful Friends: Tools and Resources for Indian Investors

So far, you’ve learned how mutual funds work, why they’re great for beginners in India, and how fund managers make smart investment choices on your behalf.

Now it’s time to take the next step — using tools and resources that help you become a smarter investor.

This section introduces you to the most useful platforms, calculators, and educational tools available to Indian investors today.

1. Online Investment Platforms

A. User-Friendly Apps for Buying, Selling, and Tracking

Apps like Groww, Zerodha, INDMoney make investing simple:

- Compare different mutual funds

- Track your portfolio anytime

- Set SIP reminders

- Read beginner-friendly guides

Use apps to simplify your investing journey.

For example:

Let’s say you want to invest ₹2,000/month in a mutual fund. With these apps, you can search for top-performing funds, read reviews, set up a SIP in just a few taps, and even track how your money grows over time — all from your phone.

B. Features Offered by Different Platforms and Direct Plan Advantages

Look for:

- Low-cost direct plans

- Free SIP tracking

- Portfolio analysis

- Tax-saving options

Choose platforms that offer both ease and value.

For example:

Some platforms let you invest in direct plans, which means no agent commission is charged. This reduces the expense ratio and increases your returns over time. Others provide alerts or goal-based investing tools so you never miss a chance to grow your money.

2. Mutual Fund Calculators (SIP Calculators, Goal Planners)

A. Estimating Your Future Wealth

Use SIP calculators to estimate how much your investments will grow.

For example:

- ₹1,000/month at 12% returns = ₹40+ lakhs in 35 years

Plan your future by understanding how your money can grow.

For example:

If you’re planning to buy a house worth ₹50 lakh in 10 years, an SIP calculator helps you figure out how much to invest monthly to reach that goal. It removes guesswork and gives you a clear plan.

B. Planning for Specific Financial Goals

Goal planners help you figure out how much to invest for things like:

- Your child’s education

- Marriage

- Home purchase

Use calculators to turn dreams into achievable plans.

For example:

You can input details like “I need ₹20 lakh for my child’s college in 10 years.” The calculator tells you exactly how much to invest every month at a certain return rate to hit that target.

3. Official Portals: AMFI, MF Central, SCORES

A. AMFI (Association of Mutual Funds in India) for General Information

Visit AMFI to learn more about mutual funds, find certified advisors, and watch educational videos.

AMFI is a trusted source for beginner-friendly information.

For example:

If you’re confused about ELSS funds or debt vs equity funds, AMFI has easy-to-understand guides and FAQs that explain everything clearly. Their famous campaign “Mutual Funds Sahi Hai” has helped millions start investing confidently.

B. MF Central for Consolidated Portfolio View and Transactions

MF Central lets you see all your mutual fund investments in one place — even across different platforms.

Get a clear picture of your entire portfolio.

For example:

If you invested through Groww, Zerodha, and Kuvera separately, MF Central shows you all your holdings together — making it easier to track and manage.

C. SCORES (SEBI Complaints Redress System) for Investor Grievances

If you face issues with a fund house or platform, file a complaint via SCORES.

Know your rights and how to seek redressal.

For example:

Say your SIP payment was deducted but not invested due to technical issues. You can log in to SCORES, raise a formal complaint, and get it resolved quickly without stress.

4. Educational Resources: “Mutual Funds Sahi Hai” and More

A. How AMFI’s Campaign Helps Demystify Mutual Funds

The famous “Mutual Funds Sahi Hai” campaign by AMFI has helped millions of Indians understand the benefits of mutual funds through TV ads, workshops, and local campaigns.

Trust-building campaigns make investing feel safe and approachable.

For example:

Many people used to think mutual funds were risky or only for rich people. But after seeing relatable ads showing young professionals, homemakers, and small business owners investing, more Indians started feeling confident about trying it themselves.

B. SEBI Investor Awareness Programs, Blogs, and YouTube Channels

Follow:

- SEBI’s investor education programs

- Finance blogs like WiseAboutFinance

- YouTube channels like Pranjal Kamra, and Paytm Money

Learn continuously to become a smarter investor.

For example:

If you’re new to investing, watching a short video on YouTube explaining SIPs in Hindi can be more helpful than reading pages of complicated financial jargon. Blogs also give tips and real-life examples that are easy to relate to.

5. Summary of this Section

- Online platforms like Zerodha, INDMoney, Groww and Kuvera make buying, selling, and tracking mutual funds easy and convenient.

- These platforms often offer direct plans, which help you earn better returns by avoiding unnecessary fees.

- SIP calculators and goal planners help you estimate future wealth and plan for major life goals like marriage, education, or buying a home.

- Official portals such as AMFI, MF Central, and SCORES ensure transparency, security, and proper grievance handling.

- Educational content from AMFI’s “Mutual Funds Sahi Hai” campaign, SEBI awareness programs, finance blogs, and YouTube channels helps you stay informed and grow as an investor.

Using these tools makes your mutual fund journey smoother, safer, and more rewarding — whether you’re just starting out or looking to grow your existing investments.

IX. Growing Your Wealth: Beyond the Basics & India’s Investment Future

You’ve learned how mutual funds work, how fund managers make smart choices, and how to start investing as a beginner in India.

Now it’s time to go beyond the basics — this section will help you grow your wealth more wisely by reviewing your investments, understanding taxes, and keeping up with how mutual funds are evolving in India.

1. Regularly Review Your Investments

A. Checking if Funds Still Align with Goals

Your life changes over time — maybe you got a new job, bought a house, or started a family. When that happens, your financial goals might change too. That’s why it’s important to review your mutual fund portfolio every 6–12 months and see if it still matches what you’re saving for.

Adjust your investments as your life evolves.

For example:

Let’s say you invested in an equity fund when you were young and single. Now, you’re married and planning to buy a home in 5 years. You may want to shift some of your money into safer debt funds so it doesn’t get affected by market ups and downs.

B. Making Adjustments (Rebalancing) as Life Changes and Markets Evolve

As you get closer to your goal, you should reduce risk. This means moving some of your money from high-risk equity funds to safer debt funds — a process called rebalancing.

Rebalancing protects your gains and reduces volatility.

For example:

Imagine you had ₹10 lakh invested entirely in equity funds when you were 30. At 45, instead of staying 100% in equities, you might move ₹3 lakh into debt funds to protect your money as retirement gets closer.

2. Understanding Taxation on Mutual Funds in India

A. Capital Gains Tax (Short-Term vs. Long-Term)

When you sell your mutual fund units, you may have to pay tax based on how long you held them:

- Equity funds: If you hold them for more than 1 year, gains above ₹1 lakh are taxed at 10%

- Debt funds: If you hold them for more than 3 years, gains are taxed at 20% with indexation (which helps reduce tax)

Knowing this helps you plan better and keep more of your profits.

Know the tax implications to maximize post-tax returns.

For example:

If you invested ₹1 lakh in an equity fund and sold it later for ₹1.5 lakh, your gain is ₹50,000 — which is below ₹1 lakh, so no tax. But if you made ₹2 lakh profit, only the amount above ₹1 lakh (i.e., ₹1 lakh) would be taxed at 10%.

B. Dividends and Their Taxability

Earlier, dividends from mutual funds were tax-free in your hands. But now, they are taxed as income, based on your income tax slab.

Dividends are no longer tax-free — factor this into your planning.

For example:

If you receive ₹20,000 as dividend income in a year and fall under the 20% tax bracket, you’ll need to pay ₹4,000 as tax on that amount.

3. The Evolving Landscape of Mutual Funds in India

A. More Indians Embracing Mutual Funds Over Traditional Assets

More people in India are choosing mutual funds over traditional options like fixed deposits (FDs), gold, and PPFs because they offer better returns and flexibility.

Mutual funds are becoming a preferred choice for smart wealth creation.

For example:

Instead of keeping all their savings in FDs, many salaried professionals are now investing in SIPs through apps like Groww and Zerodha to grow their money faster than before.

B. Technology Making Investing Smarter and More Accessible

Thanks to mobile apps, AI tools, and online platforms, investing has become easier than ever. Even first-time investors can compare funds, track performance, and manage their portfolios from their phones.

Technology is empowering everyday investors.

For example:

You can use an app like INDMoney or Kuvera to invest, track, and rebalance your portfolio — all from your phone, without visiting any office.

C. What This Means for You: Opportunities for Smarter Wealth Creation

With better access to information, lower fees, and more transparency, there’s never been a better time to invest in mutual funds in India. You can start small, stay consistent, and benefit from modern tools and expert management.

Leverage today’s resources to build a stronger financial future.

For example:

Just like millions of others, you can begin with a ₹500/month SIP, learn along the way, and gradually increase your investments as you grow more confident.

4. Summary of this Section

- It’s important to regularly review your investments and adjust them as your life changes — whether it’s a new job, marriage, or nearing your goal.

- Knowing how mutual fund taxation works helps you save more after-tax and avoid surprises.

- Dividend income is now taxable, so it’s important to include it in your investment planning.

- More Indians are turning to mutual funds over traditional assets like FDs and gold because of better growth potential.

- Technology has made investing smarter and easier — with apps, automation, and education just a tap away.

- These changes mean you have more opportunities than ever to build wealth safely and smartly.

Now that you understand how to manage your investments, review them, and take advantage of today’s tools, you’re well on your way to becoming a confident investor.

Keep learning, stay consistent, and let your money grow!

X. Conclusion – Your Investment Journey Starts Now!

Mutual funds are one of the best ways for beginners in India to grow their money with ease and confidence. They offer professional management, diversification, affordability, and the power of compounding — all while being simple to understand and invest in.

Whether you’re a student, a working professional, a homemaker, or a business owner, mutual funds open the door to financial growth that traditional options like fixed deposits simply can’t match. With tools like SIPs, you can start small and still build meaningful wealth over time.

The Indian investment landscape is changing fast, and more people are turning to mutual funds for better returns and long-term security. Thanks to technology, investing has never been easier — you can manage everything from your phone, track performance in real-time, and make informed decisions with the help of trusted platforms and regulators like SEBI and AMFI.

If you’ve been waiting for the right time to begin, now is it. There’s no need for large sums or expert knowledge. Just a small, consistent effort each month can lead to life-changing results in the future.

So take the first step today. Explore your goals, assess your risk, choose the right fund, complete your KYC, and start investing. Your future self will thank you for it.

Happy investing! 👍

XI. Frequently Asked Questions (FAQ) About Why Mutual Funds Are Ideal For Beginners In India?

1. Is it safe to invest in mutual funds in India?

Yes, mutual funds in India are regulated by SEBI, ensuring transparency and investor protection. While they carry some risk depending on the type of fund, they are generally safer than direct stock investing.